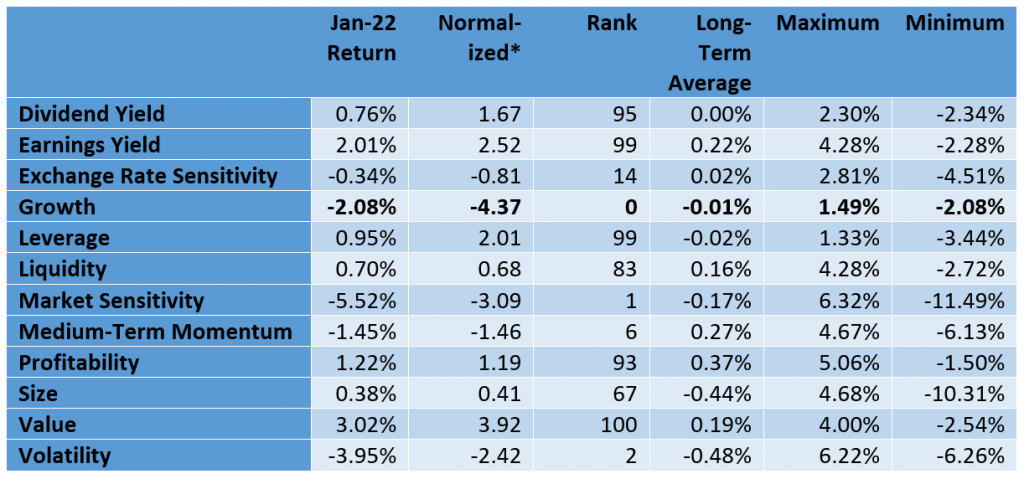

After a year of factors performing generally in line with expectations, more US model factors are now producing returns that fall into the top or bottom 15% of monthly values recorded since the model’s inception—a pattern we have not seen since November 2020. At the same time, returns to factors that are typically compensated (e.g., we expect a positive return for Value) were more likely to be in the expected direction, except for Growth, which had its worst month since 1982, and Medium-Term Momentum, which also had a highly negative month, reversing the positive trend we saw in 2021.

Investors looked for cheapness. Monthly returns for Dividend Yield, Earnings Yield and Value were among the best those factors have ever generated, coming in at 1.7, 2.5 and almost 4 standard deviations above their long-term averages, respectively. Investors also sought Profitability but shunned high Market Sensitivity and high Volatility. Those factors’ returns were historically low, too.

One factor that may have impacted portfolio returns to an unexpectedly large degree is Leverage. Highly leveraged names saw high returns in 2021, and that has continued this year, as the monthly return fell into the 99th percentile relative to its history, and was two standard deviations above average.

As we noted in our Weekly Highlights , small-cap stocks—as measured by the Russell 2000 index—gave back all of their 2021 gains. The Size factor, which holds all other factors and industry exposures constant, showed only a modestly positive return.

As markets retreated and equity volatility rose over the past few weeks, the good news is that certain defensive, value-oriented strategies did unusually well. Investors who count on the long-term anomaly of lower volatility and beta stocks faring better than their counterparts were also rewarded. The bad news, of course, is the reversal of Momentum and Growth, both of which were strong performers in 2021, but gave back a lot of those gains this year.

Source: Qontigo