Axioma’s upgraded Canada model (CA4) includes several new style factors (Dividend Yield, Earnings Yield, Profitability), almost all of which appear in other version 4 models, as described in our earlier blog post (see here).

In addition to those factors, we have added two others that reflect the unique composition of the Canadian economy: residual gold sensitivity and residual oil sensitivity. These two factors measure the sensitivities of all stocks’ industry-residual returns to Gold and Oil prices. The factors reflect the economic importance of the two commodities in the Canadian market and 1) the fact that even companies in an industry tied to the commodity (such as Oil, Gas and Consumable Fuels) may have different sensitivities to it, and 2) the potential impact of the commodity on other industries.

It is important to note that these exposures are net of industry, thereby eliminating the potential collinearity that would come from straight raw exposures. We believe this net-of-industry calculation is more intuitive. We also find that there is a risk premium associated with these factors, and that they are good candidates for applying constraints, as they occasionally have very large returns.

Exposures

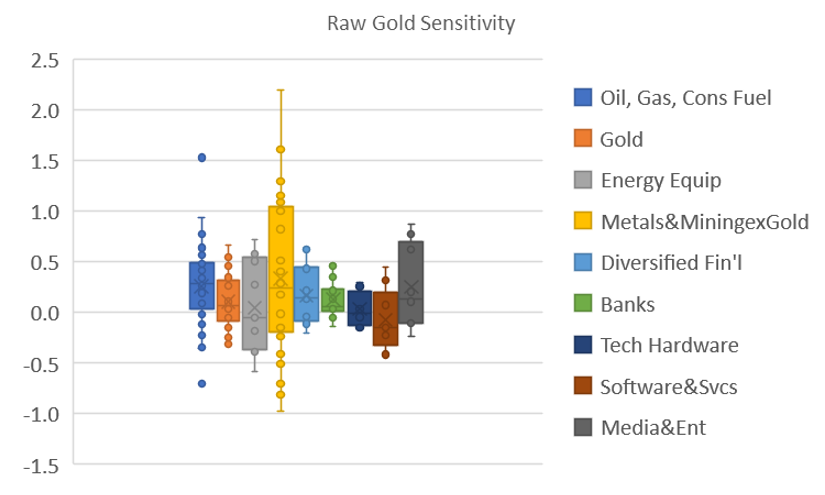

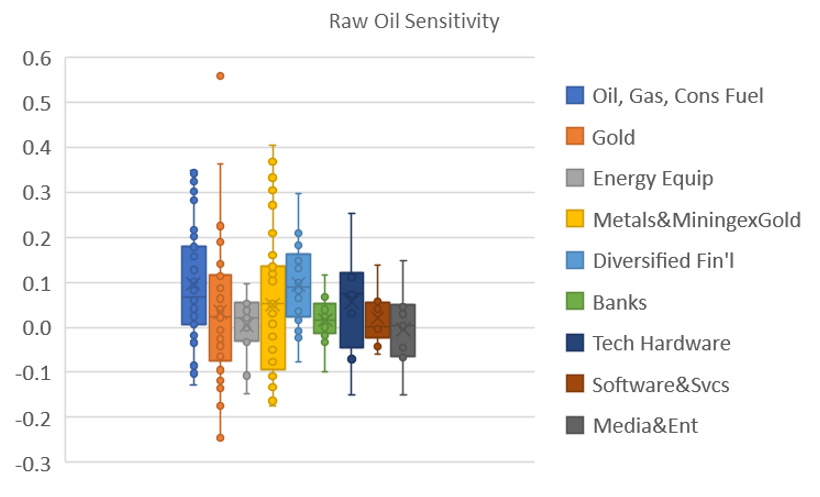

The charts below show the distribution of raw exposures to the two factors for a few selected industries. It is clear that companies outside the oil- and gold-related industries can also be sensitive to the prices of those underlying commodities.

In general, the range of raw Gold sensitivities is larger than that of oil sensitivities. In other words, some companies can be expected to see fairly big moves in their prices in tandem with, or in the opposite direction of, Gold prices.

The widest range of residual Gold sensitivities by industry could be seen in Metals & Mining ex-Gold, but most of our sample industries had some exposure. Energy Equipment and Media & Entertainment had the highest interquartile range of exposures (represented by the box). Even the Gold industry itself had some positive and some negative residual exposures.

Raw residual exposures to Oil may be of smaller magnitude than those to Gold, but here, too, we see that some companies in a given industry may have positive exposures (so benefit when oil prices rise over and above the impact of the commodity’s price move on the asset’s industry), whereas others have negative exposures. Oil, Metals & Mining ex-Gold and Gold all had a wide range of exposures, but even Technology Hardware showed a range of positive to negative exposures.

Risk and Return Characteristics

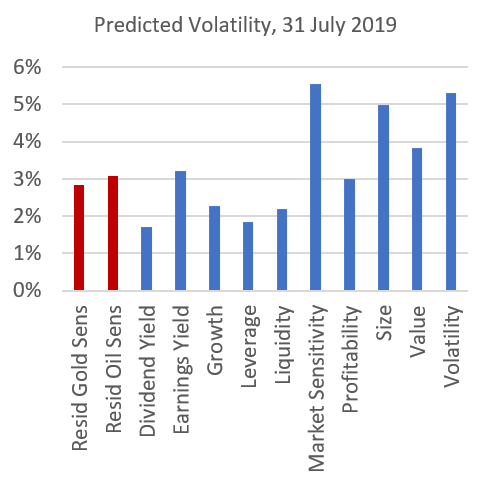

Predicted volatility of the factors, at least recently, is comparable to that of other style factors (see following chart), and much less than that of either the Gold or Oil industry factors. Monthly returns have occasionally, albeit infrequently, been outsized, however.

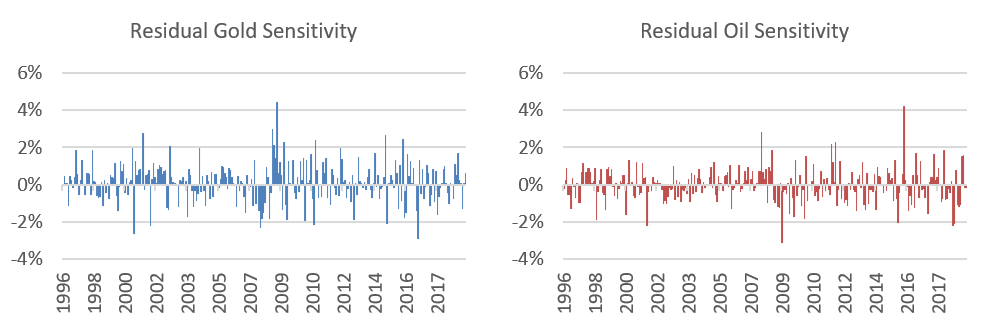

The charts below show monthly returns to the two residual sensitivity factors. The Residual Gold Sensitivity factor has a positive premium associated with it, averaging returns of more than 1% per year. While most other factors in the CA4 model have higher magnitudes of return, 1% is certainly enough to qualify the factor as one that could impact a portfolio.

The charts below show that monthly returns to Residual Gold are typically well within the range of -2% to +2%, but the return exceeded 4% in December 2008 and was almost -3% in November 2016. Residual Oil Sensitivity, in contrast, loses about 50 basis points a year on average, although it, too, has seen some big monthly returns: -3.1% in March 2009 and +4.2% in January 2016.

For both factors, the occasional large-magnitude returns for a one-month period suggest a model user may want to constrain exposures to avoid a big hit to the portfolio from a factor the manager does not have a view on.