The EURO STOXX 50® ESG Index was launched last year as an environmental, social and governance (ESG) version of the EURO STOXX 50® Index, the blue-chip Eurozone benchmark. The ESG index incorporates both standard exclusions and integrates companies’ ESG scores into stock selection. In other words, it excludes companies engaged in controversial activities and those with low ESG scores, and replaces them with the largest non-controversial company in the same sector with a higher ESG score.

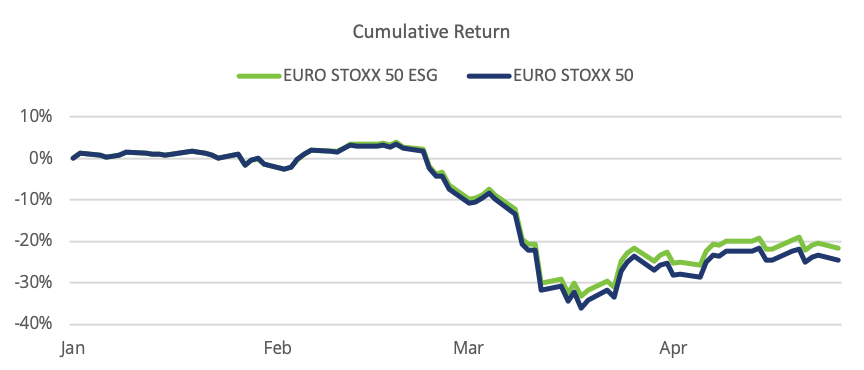

Since inception, the ESG version of the EURO STOXX 50 index has experienced both risk and return similar to that of the standard index.

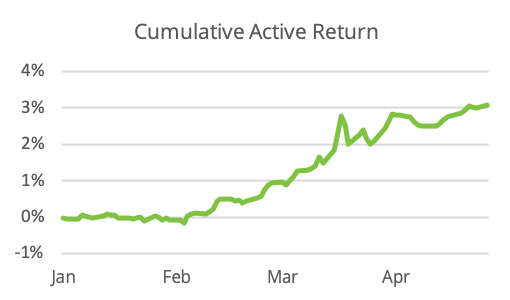

This year, although both indices fell along with the market, the ESG version outpaced the standard index by more than 300 basis points. This return is particularly noteworthy given the predicted tracking error of just over 1% on average during the period.1

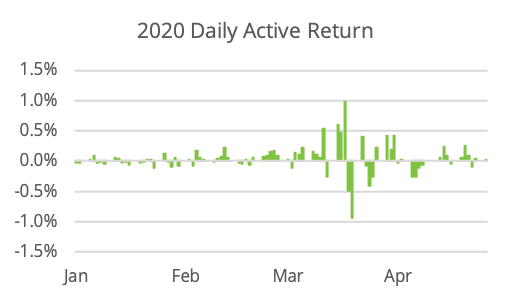

After keeping pace with the benchmark throughout January, the EURO STOXX 50 ESG Index started to outperform by a small amount on most days in February. Daily active returns became somewhat more volatile in March, but overall the ESG index beat the EURO STOXX 50 on the majority of days. The outperformance has continued in April even after the market stabilized.

Exhibit 1 – EURO STOXX ESG 50 versus EURO STOXX 50

Exhibits 2 and 3 – EURO STOXX ESG 50’s active returns

Source: Qontigo. Gross Returns in EUR.

Attribution shows little impact from style factors, where active exposures tend to be quite small. The active return was instead largely related to ESG exclusions, especially in the Aerospace & Defense and Beverages & Tobacco industries. Additional analysis shows that it was underperformance of these excluded stocks (compared to their ESG replacements) that drove the ESG index’s outperformance.

Was it the ESG selection that won out in a market dominated by a global pandemic? This time the ESG criteria weeded out names that were hurt badly by the coronavirus and replaced them with companies that performed relatively better. Over the long term, we expect ESG screens to allow us to mitigate the impact of other types of disasters — those that may be health-related, environmental, or otherwise.

1 Realized tracking error was somewhat higher than predicted, as we have observed across numerous portfolios of all kinds. We wrote about this phenomenon in a recent blog post.