A study of style factor returns for Axioma’s Asia ex-Japan (APxJP) fundamental variant risk model reveals some potential investment opportunities for factor-based managers investing in the region1.

Notably, the magnitudes of returns, both absolute and risk-adjusted, for a number of factors is high, in some cases higher than in most or all other regions for which we have released a version 4 model. The upshot is that quite a few of these risk factors can also be used as return generators to create smart beta portfolios, run quantitative strategies or add some “oomph” to fundamentally based approaches.

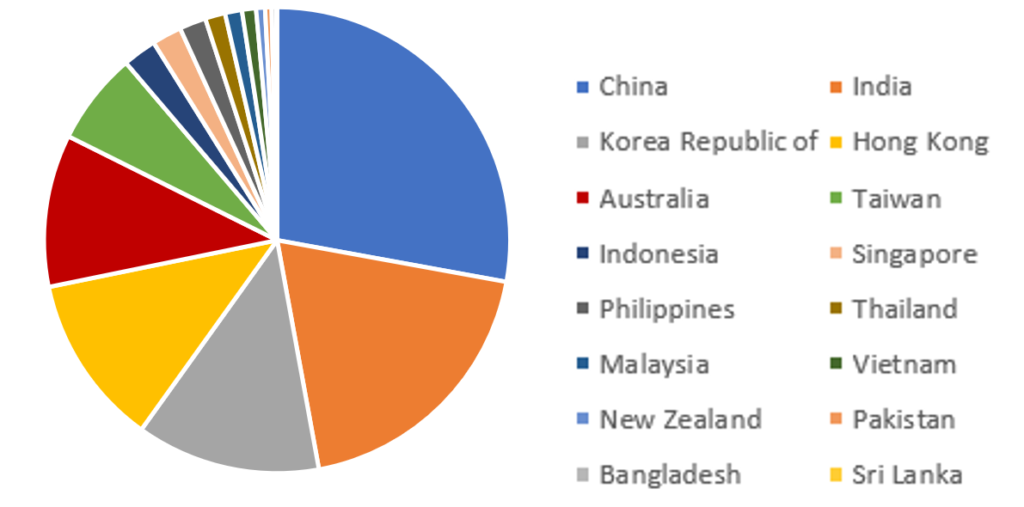

Exhibit 1 shows the breakdown of countries comprising the estimation universe at the end of 2018. The estimation universe is dominated by China, India, South Korea, Hong Kong and Australia, although a number of other, mainly emerging market, countries are represented. This breakdown helps us compare the APxJP model’s returns to those in other regions for which we have risk models, specifically China, Australia and Emerging Markets.

Exhibit 1. Asia-Pacific ex-Japan Model Estimation Universe, as of December 2018

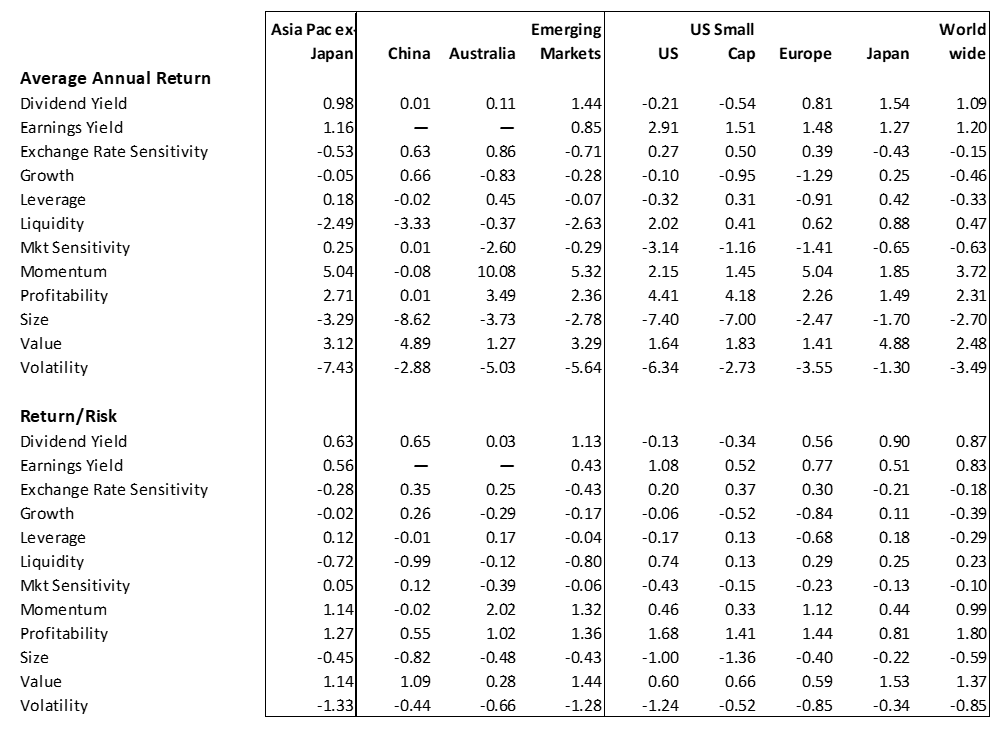

Table 1 highlights annualized absolute and risk-adjusted returns from January 1999 through December 2018 for the risk premia in the APxJP4 model. In many cases these returns show that Asia ex-Japan is a good region in which to harvest risk premia for a number of factors, including high Dividend Yield, high Earnings Yield, low Liquidity, good Momentum, high Profitability, small Size, high Value and low Volatility—in fact most of the style factors in the model. In addition, Exchange Rate Sensitivity produced a negative return of which investors should be aware.

The return to Volatility in this region, -7.43 was the most negative among the nine regions for which we have released version 4 models, and risk-adjusted return was also the highest in magnitude. Volatility also had the highest magnitude return within the list of APxJP factors. This means that low Volatility stocks fared far better than their higher Volatility counterparts, and there was more than one unit of return for each unit of risk. Interestingly, whereas, like Volatility, Market Sensitivity (a new factor in the model) produced negative returns in most regions, the return was positive (although small) in APxJP. Therefore, while the factor is a good source of understanding portfolio risk, that risk seems to go uncompensated.

In contrast to Market Sensitivity, the other three new factors in the model — Dividend Yield, Earnings Yield and especially Profitability — do seem to compensate investors for taking on the risk of investing in them. While Dividend Yield and Earnings Yield risk-adjusted returns were somewhat muted, Profitability produced the second-highest return/risk ratio with APxJP, after Volatility.

Another interesting factor was Exchange Rate Sensitivity, which measures the sensitivity of stocks to changes in their local currency, relative to the Special Drawing Rights asset. In the US, Europe, Australia, and China, the long-term average return to this factor is small but positive, meaning that stocks with positive factor exposures (typically importers) tend to outpace those with negative exposures. In Japan, Emerging Markets and for the Worldwide model, along with Asia ex Japan, the average return is negative. But don’t let the low average return fool you. There have been calendar quarters where the factor return in APxJP was as low as -3.4% and others in which the return was almost 2.0%. This suggests managers should limit their exposure to this factor, or at least examine how it may have affected returns.

Over time, illiquid (low Liquidity) stocks in APxJP (and China and Emerging Markets) tend to outperform their more liquid counterparts, and the associated return/risk ratio is fairly high in those regions. This may be a difficult or undesirable factor to target, but this highly negative average return suggests seeking liquidity may be a losing proposal. Managers will have to determine whether the lower transaction costs for more liquid names will offset the potential negative contribution from the Liquidity factor.

Growth’s return over time is close to zero in APxJP. With the exception of Japan and China, the factor’s return is negative elsewhere, especially in Europe.

The long-term average return to Size is negative across all regions. Although APxJP does not particularly stand out with a higher or lower return compared with other regions, the magnitude of return within the region is high. Similarly, Value’s return has been positive, with a high level of reward-to-risk; among regions only Australia has experienced a relatively low return/risk ratio.

Although Medium-Term Momentum does not work in China (A-Shares in Axioma’s CN4 model), it produces strong returns elsewhere, and its absolute and risk-adjusted returns are quite high in APxJP, among the three highest across the regions.

So, to summarize, on top of users’ enhanced ability to manage portfolio risk with the new Axioma APxJP4 models, they also have the opportunity to use the model to harvest risk premia with an effectiveness that may rival that in other regions.

Table 1. Annualized Long-Term Average Factor Returns and Return/Risk Ratios for Axioma’s V4 Models

1The study was conducted following the release of Axioma’s latest (Version 4) risk models for Asia-Pacific and Asia-Pacific ex-Japan.