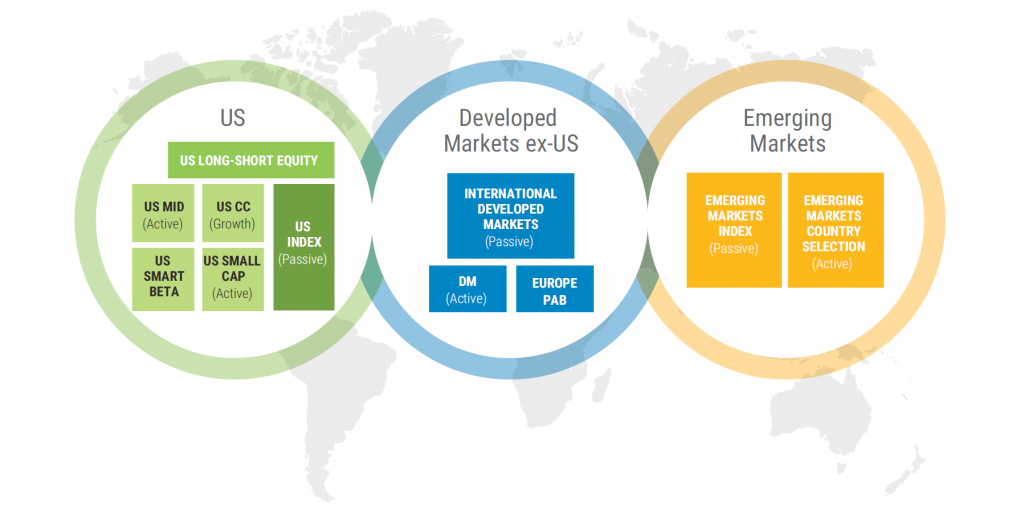

The Axioma Worldwide Equity Linked Factor Risk Model (Linked Model) combines the Axioma United States Equity Model (AXUS4) with the Axioma Developed Markets ex-US (AXDMxUS4) and the Axioma Emerging Markets (AXEM4) Models into one interconnected equity model.

The Challenge for Global Asset Allocators

Global risk models offer the convenience of a single model, but they may also miss local factor nuances and key diversification benefits available between different markets that are important to understand total global equity risk, relative to a policy benchmark or in absolute terms. The only available alternative was to use several individual regional models to capture these nuances – impractical from a cost and efficiency perspective.

The Solution

With full coverage of global markets but a regional factor structure that recognizes the differences in factor phenomena from one market to another, the model enables users to drill down within regional allocations to understand the factors driving portfolio performance and risk while simultaneously allowing aggregation of these allocated risks up to the total global equity allocation of the fund.

A Global Model with Regional Drill-Downs

Understand what’s driving the total plan equity allocation.

Discretionary Hedge Funds:Don’t sacrifice accuracy in the name of coverage

Risk models are often built for a long-only world that fits neatly into geographic segments. This results in a poor fit to investing approaches unconstrained by client-driven mandates. Many managers have no choice but to compromise by using a global model offering full portfolio coverage at the expense of the factor granularity offered by regional or single country models where the majority of their positions trade.

Global Asset Managers:One equity risk model for portfolio construction and risk management

Portfolio managers assigned to domestic or regional mandates may use a risk model estimated from the particular geographic region corresponding to their mandate while those tasked with monitoring firm-wide risk and performance used a more generalized risk model to ensure they are able to capture all the firm’s portfolios.

Global Quant Funds:Better estimates of global equity risk through regional sub-models

Traditional global equity models have to make assumptions regarding the homogeneity of factor behavior over a set of disparate local and regional markets. However, markets trading at different times during the day representing different investment opportunities sets create unique factor behaviors in each market. A generalized model of global equity may average this factor behavior which can have consequences in terms of risk forecast accuracy as well as risk-adjusted performance.