- Treasury curve steepens as Fed discounts ‘jumbo’ hike

- Stagflation fears weigh on pound

- Continued stock-bond sell-off offsets lower equity and FX volatility

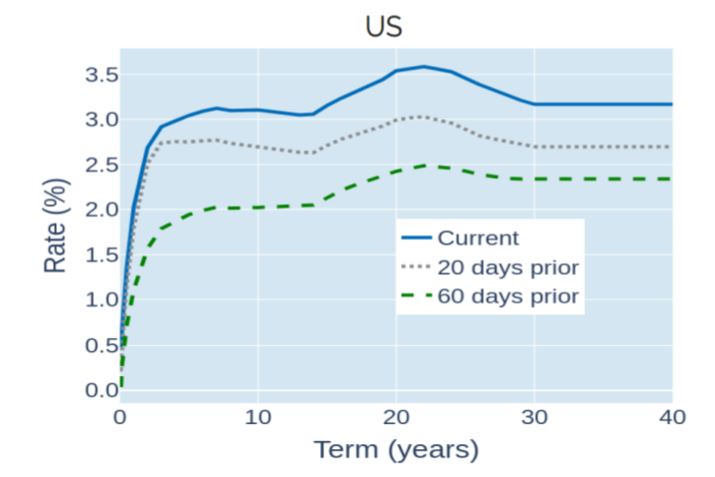

Treasury curve steepens as Fed discounts ‘jumbo’ hike

The 10-year US Treasury yield edged above 3% for the first time since November 2018 in the week ending May 6, 2022, as the Federal Reserve raised its target rate corridor by half a percentage point, while hinting that “additional 50 basis point increases should be on the table at the next couple of meetings.” However, when questioned about whether a move of 0.75% or more was possible, too, Chair Powell replied that this was “not something the committee is actively considering.” As a result, the monetary policy-sensitive 2-year rate remained unchanged, whereas longer rates soared between 24 and 33 basis points, as labor-market data released on Friday showed continuing strong jobs and wage growth, which heightened concerns over persistent inflationary pressure.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated May 6, 2022) for further details.

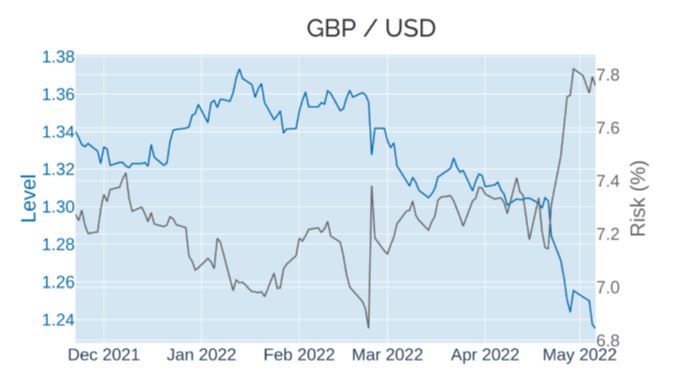

Stagflation fears weigh on pound

The pound sterling slumped to its weakest level against the US dollar in almost two years in the week ending May 6, 2022, after warnings from Bank of England rate setters at their monthly meeting on Thursday that UK GDP “is projected to fall in 2022 Q4”, while CPI inflation is expected to peak at slightly above 10% in the same period. At the same time, the meeting minutes underlined “the primacy of price stability in the UK monetary policy framework”, indicating that the Monetary Policy Committee is likely to continue raising rates in line with market expectations, while considering beginning “the process of selling UK government bonds held in the Asset Purchase Facility.” In a similar reaction to their American counterparts, short to medium-term Gilt yields were little changed, while longer rates climbed between 13 and 22 basis points.

Please refer to Figures 3 & 6 of the current Multi-Asset Class Risk Monitor (dated May 6, 2022) for further details.

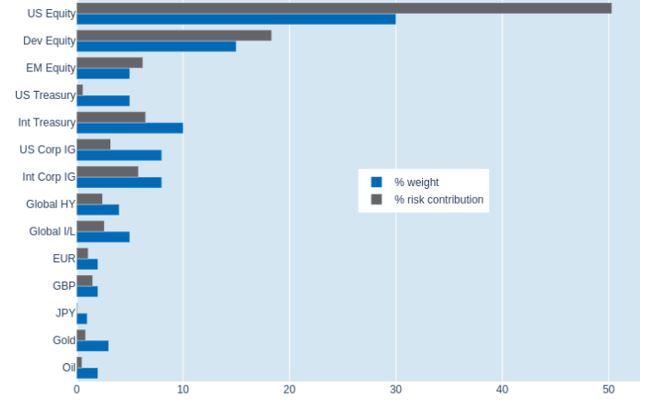

Continued stock-bond sell-off offsets lower equity and FX volatility

Predicted short-term risk in Qontigo’s global multi-asset class model portfolio dropped 1 percentage point to 11.9% as of Friday, May 6, 2022, due to a concurrent decline in FX and equity volatility, which reduced the combined percentage risk contribution of non-US developed and emerging-market shares by 4.8% to 24.5%. However, part of this was offset by the continued simultaneous sell-off in stocks and bonds, which meant that the fixed income assets in the portfolio saw their share of overall risk rise by 1.7%. Commodities and the Japanese yen, meanwhile, provided the biggest diversification benefits, due to their low correlation with most other asset classes.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated May 6, 2022) for further details.