Potential triggers for sentiment this week1 :

- US: Q2 2022 earnings season gets under way with PepsiCo on Tuesday, followed by Delta Air Lines on Wednesday, JPMorgan Chase and Morgan Stanley on Thursday, and Wells Fargo, Citigroup and PNC Financial on Friday. US inflation is expected to have risen to 8.8% in June, retail sales are seen rebounding, manufacturing production likely stalled, and the University of Michigan consumer sentiment survey is expected to sink to a new record low.

- Europe: The UK’s monthly GDP figures are expected to show the economy stalled in May. Other data include the Eurozone’s balance of trade and industrial production, Germany’s inflation figures and wholesale prices, and Italy’s retail sales and foreign trade.

- APAC: China’s GDP, retail sales and industrial production data; Australia’s labor statistics; Japan’s machinery orders.

- Global: Macro worries, a resurgence of COVID-19 infections, and the ongoing war in Ukraine will continue to affect sentiment negatively. Another potential worry for investors is the financial lifeline to President Putin from China and India through Russian oil purchases.

1 If sentiment is bearish/bullish, a negative/positive surprise on these data releases could trigger an overreaction.

Summary of changes in investor sentiment from the previous week:

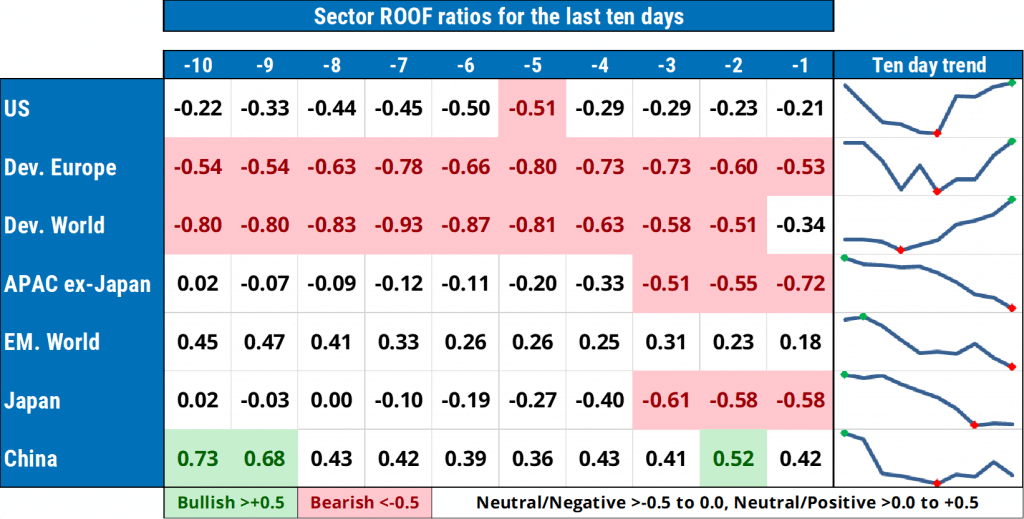

- Investor sentiment staged a recovery in most developed markets but continued to weaken in Asia ex-Japan and Japan, while managing to remain positive in global emerging markets and China. Investors in the US, Europe and global developed markets seem to be getting their affairs in order ahead of the earnings reporting season under way this week.

- Sentiment works through hopes and fears. In the US, recent fears about the strength of the economy brought about by the highest inflation levels in decades has given way to hopes that corporate earnings will come though unscathed. Wednesday’s inflation report will test investors’ faith. Meanwhile, in the background, the January 6 hearings continue.

- Sentiment in global emerging markets, Asia ex-Japan and Japan weakened further, with investors in the latter two ending last week bearish. Within an inflationary background, hopes of continued high profit margins in developed markets can only be balanced with fears of a margin squeeze among the developing world’s supply chain — in a zero-sum game, something’s gotta give.

- CEOs will have to woo, dazzle and awe their shareholders this reporting season, or else they will learn the hard way that it is sometimes easier to be an investor than to have them. Growing recession fears means the pie is getting smaller for everyone, and so for one company’s sales to be up, another one’s must be down. This reporting season will be all about one-upmanship, which should increase dispersion between winners and losers, the mother’s milk of stock pickers.

Jump to a specific market

US investor sentiment

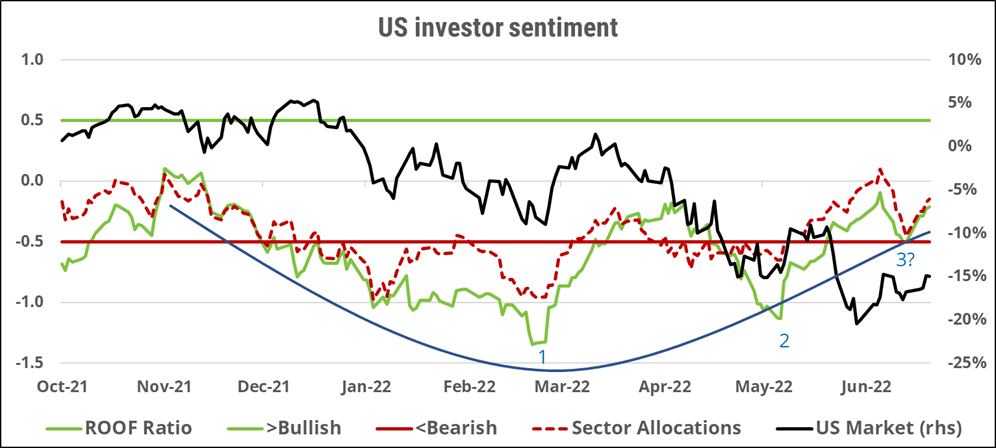

Sentiment among US investors (green line) recovered last week, erasing the previous week’s decline, and ending mildly negative. Year-to-date, sentiment has hit two bearish lows, one in early March, the second in mid-May. Each one was followed by a strong rebound in sentiment, which reversed before they could break above the high-water mark reached in November last year. On July 1, 2022, investors’ mood once again became bearish, for a single day, and started to rebound last week. Will this recovery in sentiment, starting from a higher base than the previous two lows, have the momentum to turn positive for the first time this year? The path of inflation, interest rates and the economy remain highly uncertain. Only valuations will provide some answers in the next few weeks, allowing investors to decide if a 20% haircut was too much, or not enough. In the BC — or Before COVID — era, the combination of a neutral risk appetite and a focus on stock-selection risk has in the past protected markets from external shocks as dispersion ensured there was enough diversification available for investors to de-risk their portfolios without having to run for the exit.

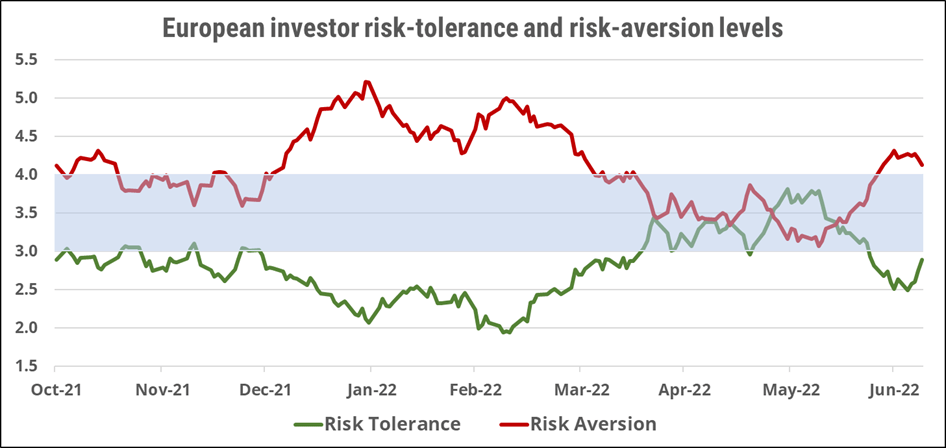

European investor sentiment

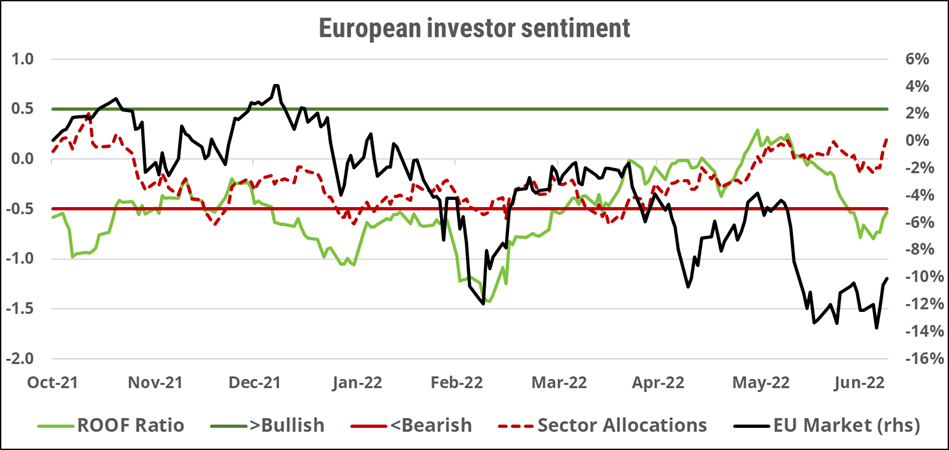

European investors’ sentiment (green line) started a recovery last week, ending still bearish but off the lows reached on Monday. Corporate earnings announcements over the next few weeks will take some of the guessing work on valuations out for investors: have markets corrected enough or is more red ink needed? Meanwhile the race is on to circumvent Russia’s oil and natural gas trump card, and replenish storage reserves ahead of the winter and avoid an energy crisis which is sure to push the continent into a deeper recession when it hits. Coal, after having been demonized by the environment lobby, has now been called out of retirement to serve in Germany, proving that even after a radical hysterectomy, some golden geese can still lay eggs. Risk appetite is not yet back to neutral, and there remains a bias towards risk-aversion among European investors. Will this week’s batch of economic and corporate data releases help to close the gap?

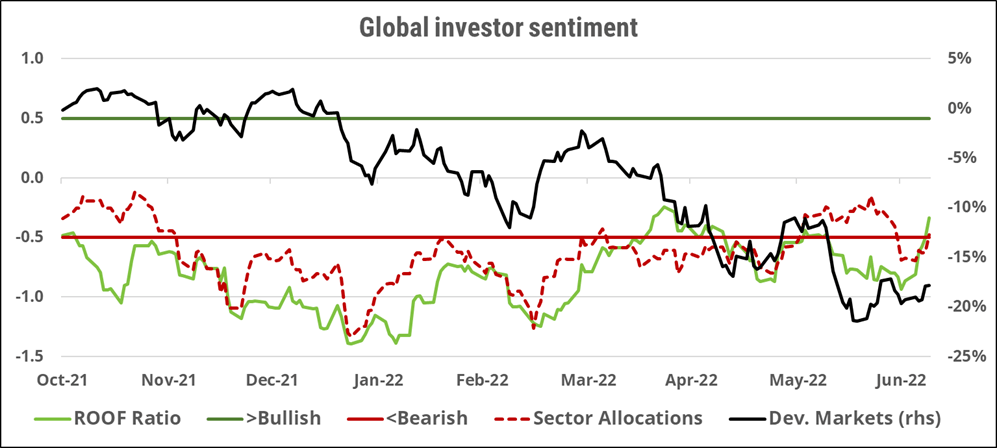

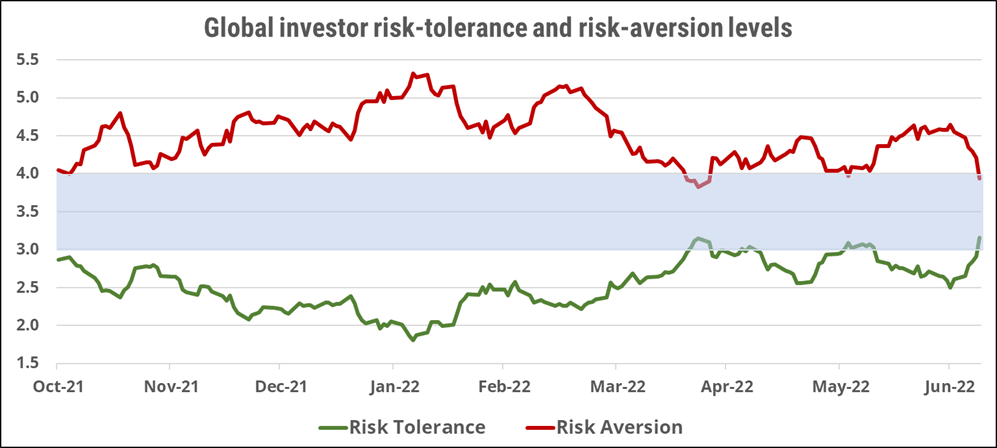

Global developed markets investor sentiment

Sentiment among global developed-markets investors (green line) recovered sharply last week from its bearish levels of the previous month. Helped by an improving mood among both US and European investors, sentiment ended the week still negative but inside the neutral zone (i.e., above -0.5) and close to its previous high-water mark of early April. Sentiment has been bearish or strongly negative for most of the time year-to-date. A break into positive territory now could signal a bottoming out of sentiment in the first half of the year and pave the way for a recovery that could enable a more sustained market rally into the second half. Uncertainty remains high, however, and many things need to go right, and others not to go wrong, for markets to stage a broad-based and sustainable recovery. Investors may discover that without the help of the ECB and with a war still raging on the region’s eastern front, the traditional summer rally this year may turn out to be an entirely different kettle of caviar. Risk appetite is almost back to neutral, the best it has been all year, but it will take a lot of positive news to get risk tolerance to rise above risk aversion in this macro environment.

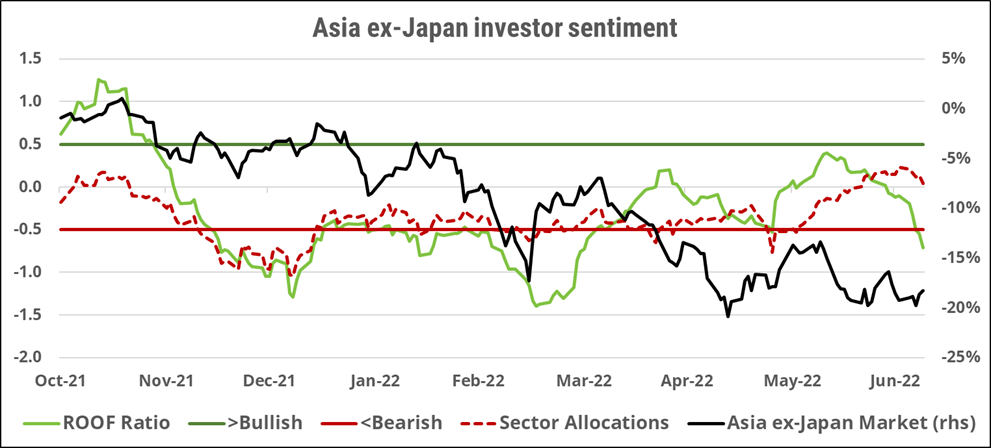

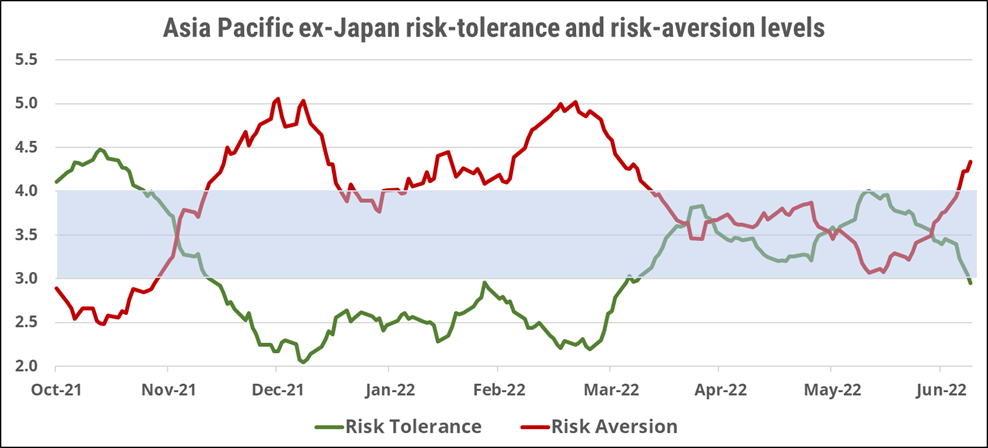

Asia ex-Japan markets investor sentiment

Sentiment among Asia ex-Japan investors (green line) deteriorated sharply last week, ending bearish for the first time since March this year. A failed payment by one of China’s real-estate companies has reminded regional investors that the macro situation is putting increasingly higher stress on both countries and companies with weak balance sheets. The prospect of global stagflation (high inflation, high interest rates and low economic growth), is a worst-case scenario for the region and one which investors are increasingly worried about. As the earnings reporting season gets under way in the US and Europe, regional investors will also find out if profit margins in the developed world have been maintained at the expense of those in Asia. This is not a case of ‘absence makes the heart grow fonder’ — Asian investors need to pay the mortgage too. They have been patient for three years now, underperforming developed markets during that time, but despite low valuations, risk aversion has been rising since late May and is now firmly in control of risk appetite.

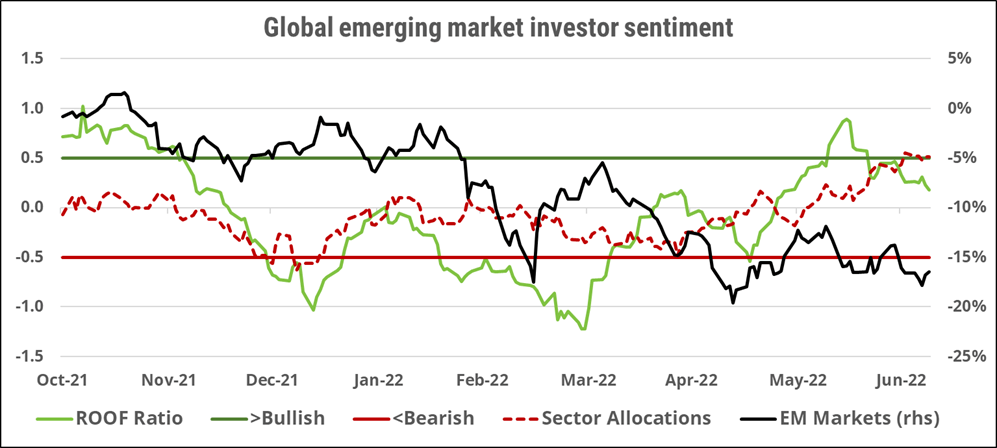

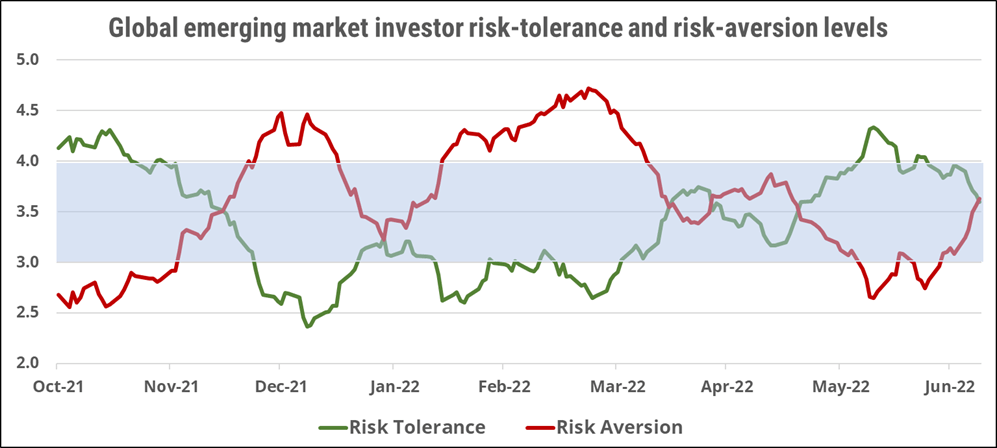

Global emerging markets investor sentiment

Sentiment among global emerging-markets investors (green line) declined slightly last week, ending just positive but well off its bullish highs of mid-May. That high was spurred by the reopening of major Chinese cities and the promise of strong fiscal and monetary stimulus for the world’s second-largest economy. Events in Sri Lanka over the weekend will have raised the contagion risk of socio-political unrest in other emerging markets due to the current macro situation (high commodity prices, high interest rates, a strong US dollar). Other pressures are coming from the increasing strain the war in Ukraine is putting on the emerging world’s food supply chain, and the still fluid COVID-19 situation in various countries. Risk appetite is now back to neutral, but risk aversion is rising faster than risk tolerance is declining, indicating that investors are getting more and more nervous.

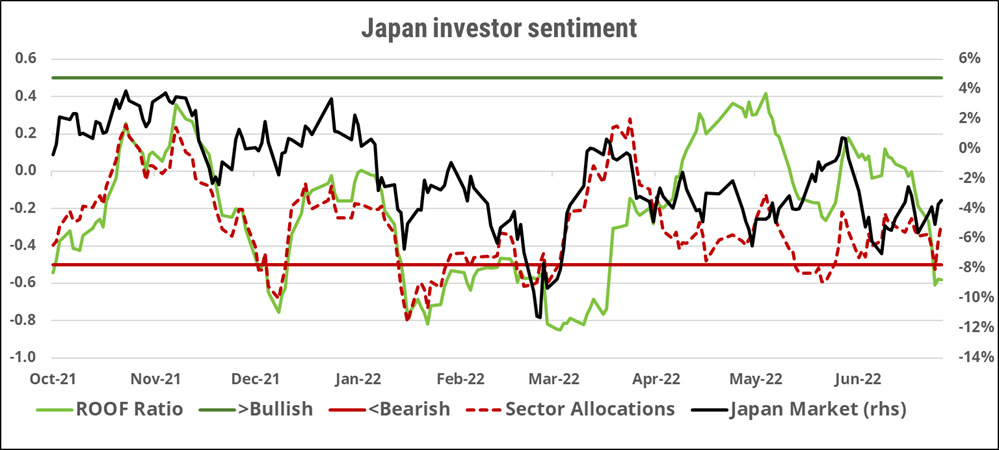

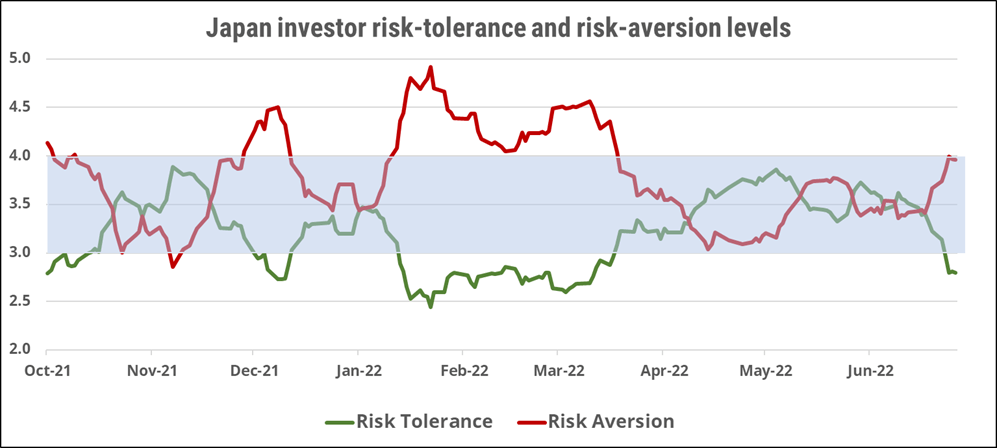

Japan market investor sentiment

Sentiment among Japanese investors (green line) continued its recent decline last week, ending bearish for the first time since March this year. The shocking assassination of former Prime Minister Abe will do nothing to reverse the fall in sentiment in the short term. Risk appetite turned negative recently, more due to a fall in risk tolerance than a rise in risk aversion, but the supply and demand for risk remains only marginally unbalanced and far less pessimistic than in February and March of this year. The BoJ remains accommodative, and investors will focus on how inflationary pressures affect domestic consumption, as well as the number of tourists who take advantage of the sharply weaker Japanese Yen during the summer holidays. Any softness in either metric will feed risk aversion and cause risk appetite to worsen. In the worst-case scenario that inflation keeps rising and the BoJ has to do its own monetary policy pivot, sentiment will worsen even further, and faster, forcing a re-test of the March market lows.

China (domestic) investor sentiment2

Sentiment (green line) among Chinese (A-shares) investors remained strongly positive last week, awaiting more details on the authorities’ reflation plans. A failed payment by one of the country’s real-estate borrowers did not seem to negatively affect domestic sentiment, which has recovered from the two-months lockdown in Q1. The strongly positive mood since early June continues to allow markets to rebound from their lows reached in mid-May, but both now require more positive news to rise higher. Risk tolerance remains above risk aversion but the gap between the two has been stable for over a month now. We may need to see more stimulus for it to widen further, keeping risk appetite steady at current levels for the time being.

2 Note that as of the end of May 2022, we have switched to using a core benchmark as estimation universe instead of the broad market portfolio to better capture the behavior of institutional investor by removing the small caps from our analysis.