Potential triggers for sentiment this week1 :

- US: Consumer confidence and personal consumption expenditures.

- Europe: ECB forum on central banking with speeches from President Lagarde, Fed Chair Powell and BoE Governor Bailey. Key reports on Eurozone inflation and unemployment.

- APAC: Japan’s Tankan Large Manufacturers Index, consumer confidence indicator, retail sales, industrial production, housing starts and unemployment. China manufacturing PMI.

- Global: G7 and NATO meet to discuss the worsening situation in Ukraine as well as how to tackle rising inflation.

1 If sentiment is bearish/bullish, a negative/positive surprise on these data releases could trigger an overreaction.

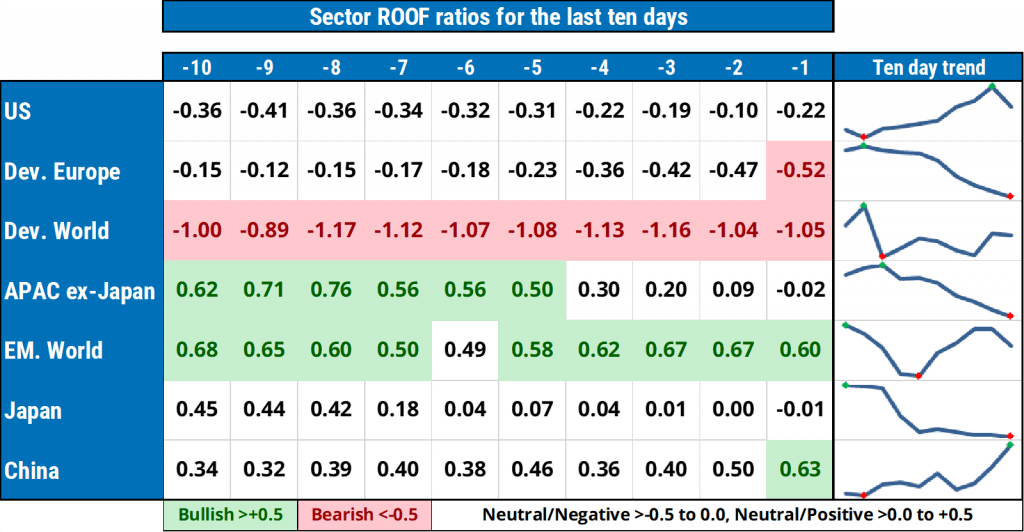

Summary of changes in investor sentiment from the previous week:

- Sentiment declined sharply last week, becoming negative in Asia ex-Japan, Japan and developed Europe, with the latter ending bearish for the first time since early April. We continue to see a divergence of sentiment between developed- and emerging-market investors, with the former remaining bearish and the latter increasingly bullish. Sentiment among US investors improved slightly but remained negative, ending on a weak note Friday after a failed recovery attempt. Sentiment in China rose further on continued reflation talks by authorities, and ended the week bullish for the first time since November 2021.

Jump to a specific market

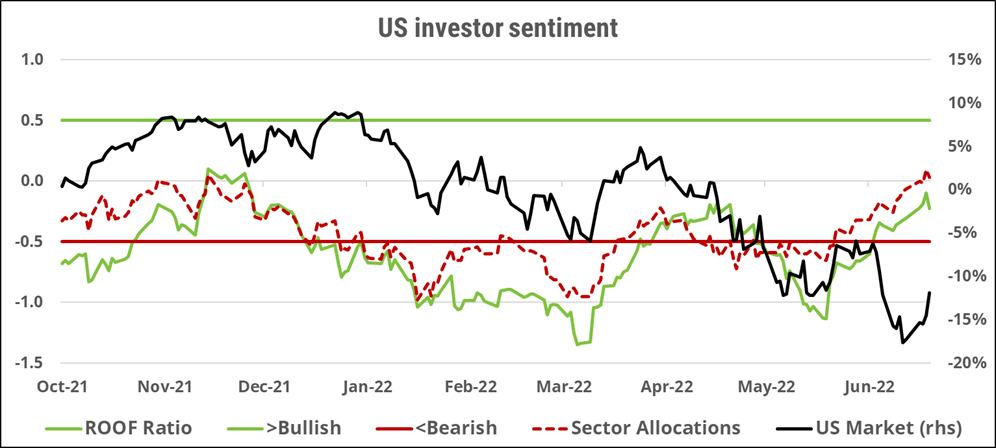

US investor sentiment

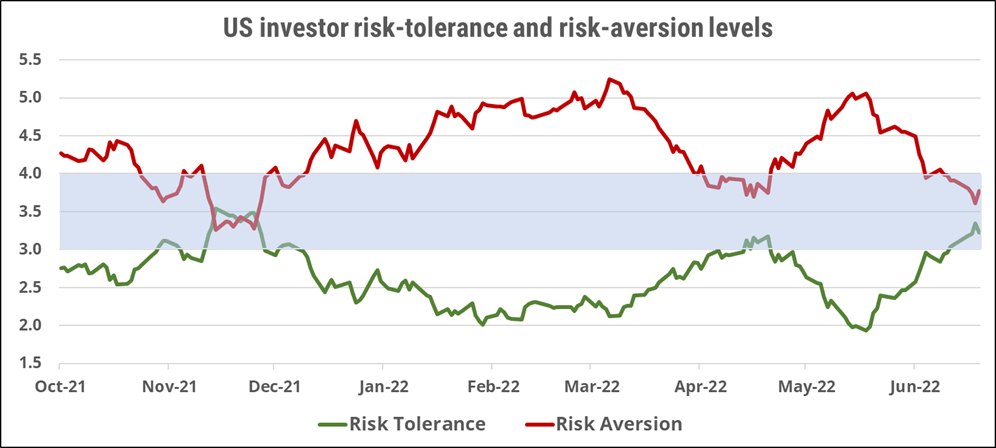

The month-long recovery in sentiment among US investors (green line) stopped last Friday, when it erased half of the previous days’ gains in a single day, still ending the week negative. Sentiment was last positive in the US in November last year, and with only macro news (jobs and inflation reports) awaiting investors between now and the start of the quarterly earnings reporting season, it will take major good news on the inflation front to give them the confidence they need and hence lift sentiment back to positive territory. Risk tolerance and risk aversion are evenly balanced right now, which should prevent an overreaction in either direction ahead of the July 4 long weekend. The war in Ukraine does not seem to be ending any time soon, meanwhile the G7 are said to be preparing a new round of economic sanctions on Russia. Given the geopolitical and macroeconomic status quo, markets are likely to remain rangebound for now.

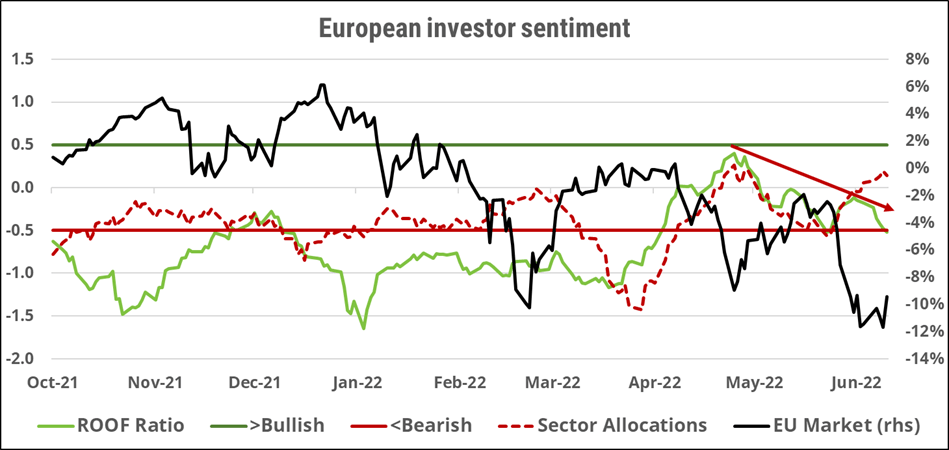

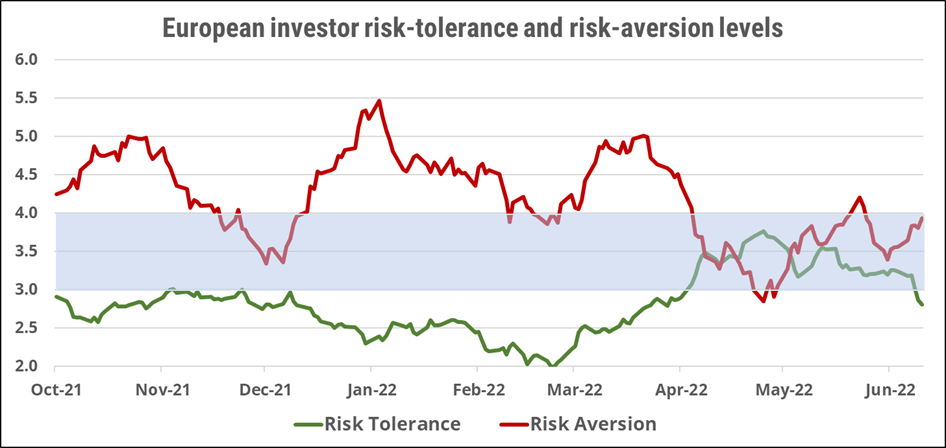

European investor sentiment

European investors’ sentiment (green line) continued its slow decline of the past two months, ending bearish for the first time since April. Following the ECB’s U-turn on inflation and monetary policy, sentiment has been on a downward path since early May and the recent increase in market volatility has only accentuated this mood swing. Interestingly, the sector allocation (red dotted line) indicates that investors are still implementing a timidly risk-tolerant strategy, implying that after the shock delivered by the latest round of inflation numbers, they may be hedging risk rather than selling it. We note that in the Kubler-Ross process, denial comes before acceptance. Sentiment is still fragile with risk-aversion rising and risk-tolerance falling, and while the two are still relatively close to each other, they appear headed in opposite directions in the near term, forewarning a growingly negative risk appetite. If the imbalance between the two grows further this week, combined with an unexpected news shock (escalation of the war in Ukraine, extreme weather event, disunity among G7 or NATO members, increase US-China tensions — take your pick), markets could see another overreaction like the one we experienced earlier this month.

Global developed markets investor sentiment

Sentiment among global developed-markets investors (green line) remained bearish last week, showing very little signs of an impending improvement. Risk-aversion levels were capped near recent highs while risk tolerance drifted a tad lower, barely registering a pulse. The increasing geopolitical tensions as well as the large dislocation in monetary policy among major central banks continues to raise the risks of multi-currency portfolios, deterring investors from taking on new positions given the high hedging costs involved. While financial crises trigger a ‘too-big-to-fail’ risk-tolerant response, macroeconomic and geopolitical crises tend to generate a ‘too-uncertain-to-call’ risk-aversion response. Global developed markets are now in a sentimentally dangerous zone and investors should err on the side of caution in the near term.

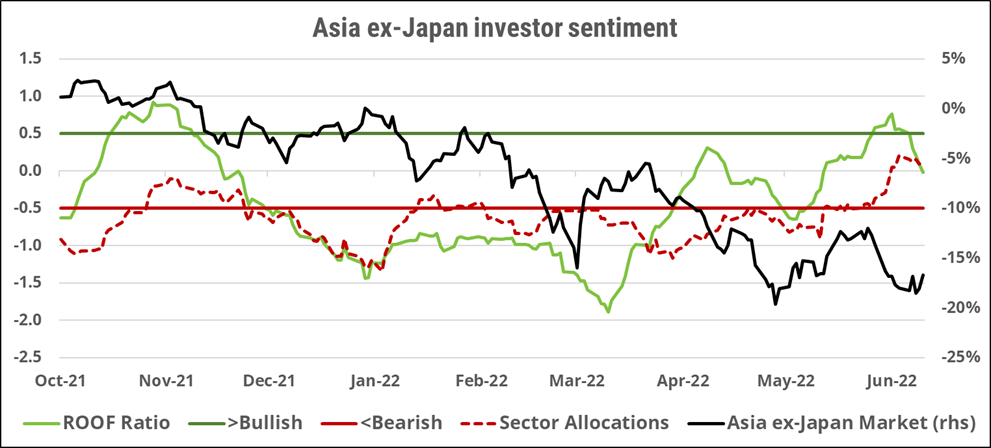

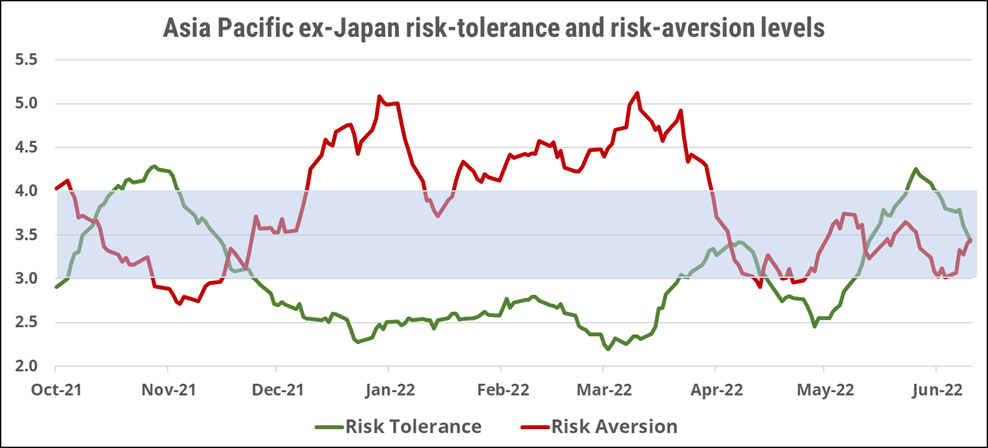

Asia ex-Japan markets investor sentiment

Sentiment among Asia ex-Japan investors (green line) failed to hold on to the bullish levels of the previous week, declining sharply last week to end negative for the first time since mid-May. The larger-than-expected US interest rate hike this month, along with the prospects of another similar-sized one at the Fed’s July meeting, has sent investors running for the sidelines. Risk tolerance declined sharply in the week, erasing all month-to-date gains, while risk aversion rose, ending the positive risk appetite that had developed since late May. Risk appetite is now back to neutral, and as valuations have remained low, it will take a strong directional news to move investors either way out of this comfort zone where they are awaiting clarity on key macroeconomic forecasts.

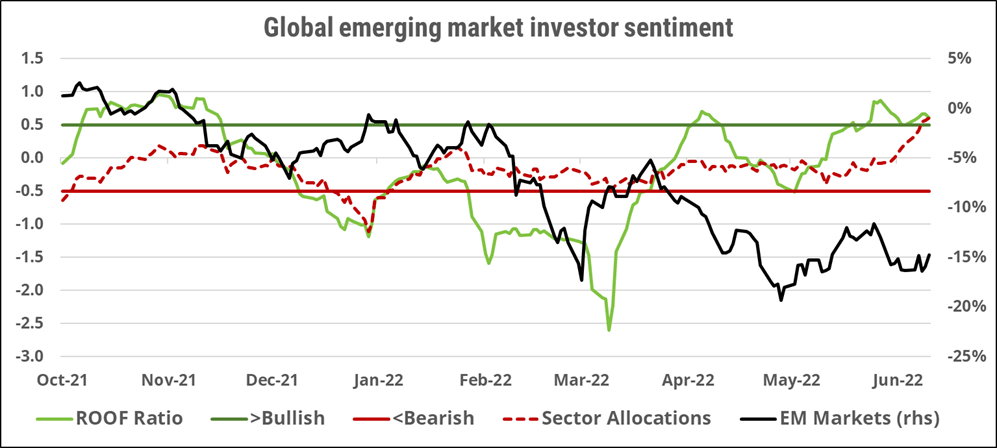

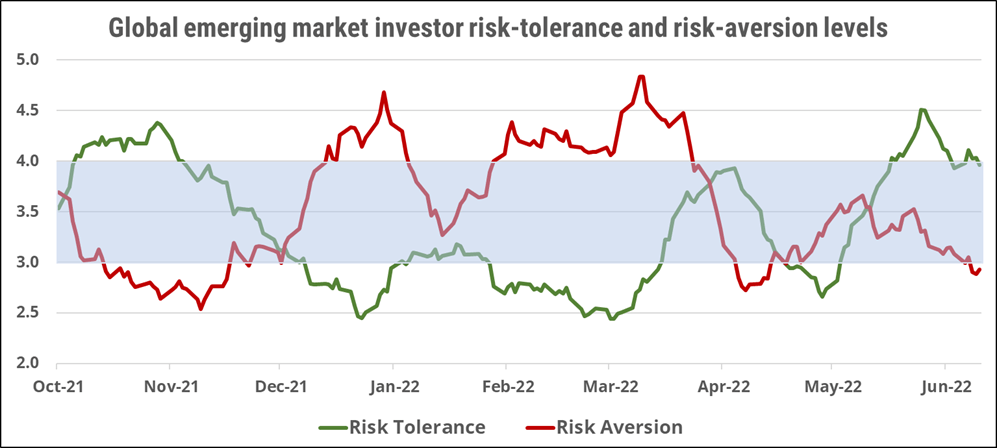

Global emerging markets investor sentiment

Sentiment among global emerging-markets investors (green line) bounced back last week, returning to a bullish level. Sector allocation (red dotted line) indicates that the implementation of risk-tolerant strategies remains more popular with investors, which has provided a floor for markets in the last four weeks. As noted recently, while risk-aversion levels have continued to decline, risk-tolerance levels made an abrupt turn in June, declining at a parallel rate with risk aversion and preventing net risk appetite from growing. Presently, valuations are still relatively low, especially when compared to developed markets, and sentiment is still bullish, which could provide strong support for markets. Risk aversion would need to rise strongly for this to change.

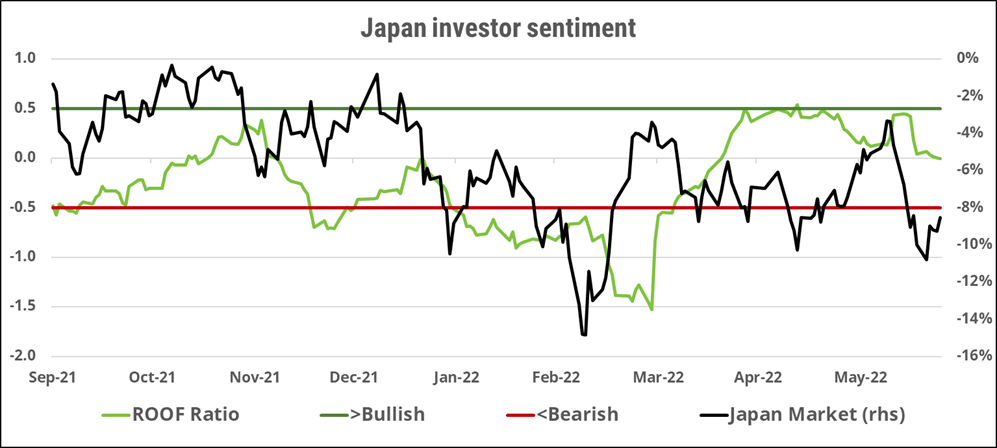

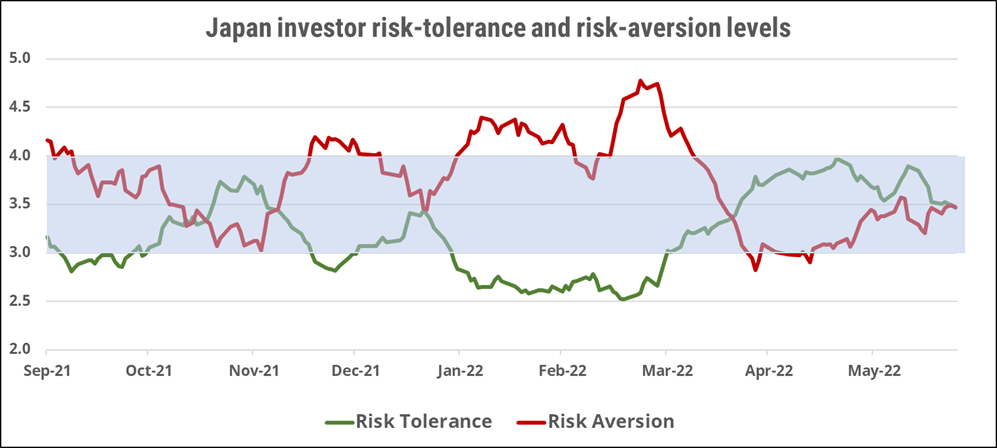

Japan market investor sentiment

Sentiment among Japanese investors (green line) ended the week neutral, erasing all of April’s and May’s positive momentum. At 135 yen to the US dollar, the positives for domestic exporters are being eroded by negatives for importers and consumers alike. Contrary to other markets, investors in Japan feel that continued stimulus by their central bank could have adverse consequences for the domestic economy instead of beneficial ones. If local consumers cut back on their spending habits, and foreign tourists fail to show up — after all, it’s been three years since they saw the Grand Canyon, visited the Louvre, or simply been to a beach closer to home, while they went to Japan for the Olympics just last year — the economy could be in for a rough landing. There is currently no imbalance between risk aversion and risk tolerance, which translates into a low potential for overreaction to news.

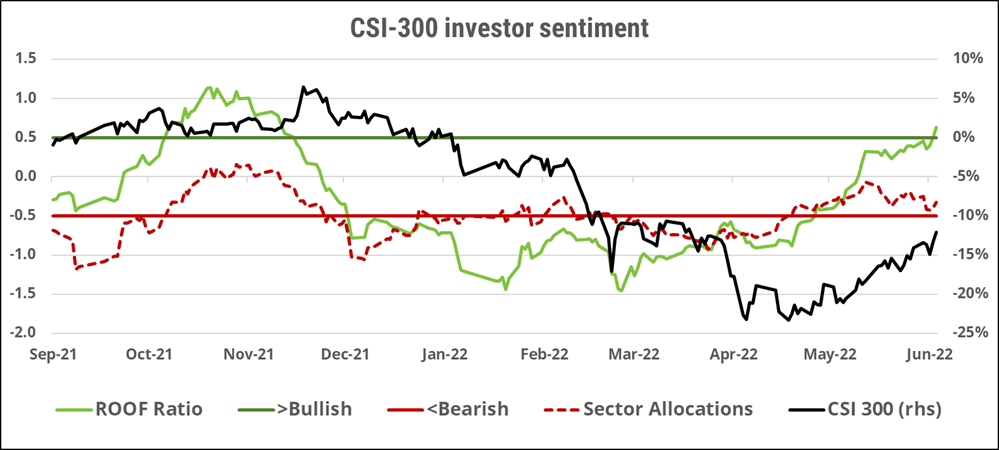

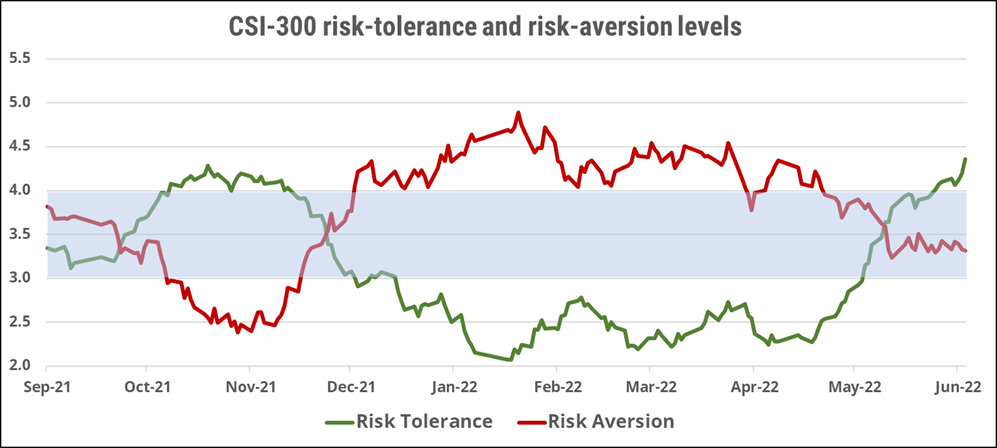

China (domestic) investor sentiment2

Sentiment (green line) among Chinese (A-shares) investors continued to rise last week, ending bullish for the first time since November last year. The combination of the country’s reopening and ongoing verbal support for the economy via planned fiscal and monetary stimulus, and the end of some regulatory restrictions on Big Tech, has helped sentiment recover since mid-March, and markets since mid-April. Risk-tolerance levels are now comfortably higher than risk-aversion levels, and still rising. We note that risk-aversion levels have stopped declining for several weeks now, and remain well above their previous lows from November 2021. This could indicate some latent geopolitical concerns related to the US-China relationship on behalf of investors. For now, domestic investors seem more willing to act on positive news than negative news.

2 Note that as of the end of May 2022, we have switched to using a core benchmark as estimation universe instead of the broad market portfolio to better capture the behavior of institutional investor by removing the small caps from our analysis.