Equity Risk Monitors

Our Equity Risk Monitors analyze index-level topline volatility and its components using Axioma’s equity factor risk models and corresponding STOXX’s market-capitalization weighted indices.

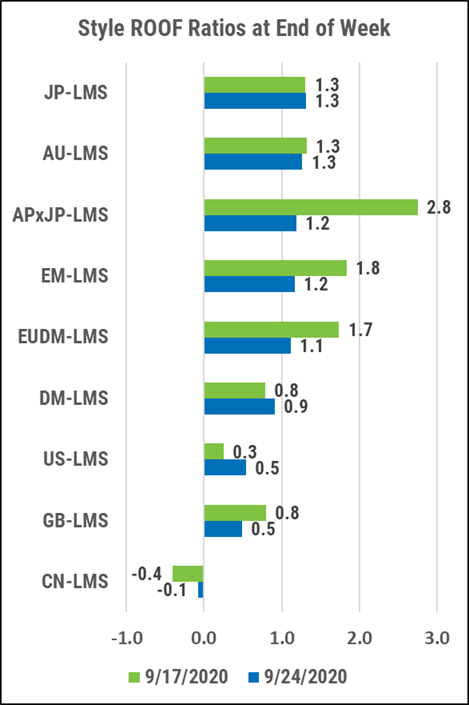

These daily reports explore the major drivers of predicted risk and offer contextual market-based data. Users can download individual charts or a PDF of the full set for each country or region.

Axioma’s Equity Factor Risk Models offer a comprehensive analysis of risk exposures with multiple views, using short- and medium-term horizons, and fundamental and statistical factor structures.

- Global Developed Markets: STOXX Developed World | STOXX Global 1800

- Developed Markets ex-US: STOXX International Developed Markets | STOXX Global 1800 ex USA

- Emerging Markets: STOXX Emerging Markets | STOXX Emerging Markets 1500

- United States: STOXX World US | STOXX USA 900

- Asia Pacific ex-Japan: STOXX Asia/Pacific 600 ex Japan

- Australia: STOXX World Australia | STOXX Australia 150

- Canada: STOXX World Canada | STOXX Canada 240

- China: China A 900

- Europe: STOXX Europe 600

- Japan: STOXX World Japan

- United Kingdom: STOXX World UK | STOXX UK 180

- US Small Cap: STOXX US Small Cap | Russell 2000

Latest Highlights