Qontigo has introduced, in collaboration with Eurex, the iSTOXX® Spread Ratio Indices, which track the relative value spread between two related securities.

Each one of 42 indices1 in the family consists of two types of stock issued by one same company, such as dual listings or different share classes. Eurex launched futures on 22 of the indices at the end of June and plans to introduce eight more contracts early next year.

The indices and associated futures enable market participants such as hedge funds to trade the spread, a popular strategy that seeks to exploit differentials in the price relationship between two legs of a pair, in a way that significantly reduces associated trading costs and risks.

The relative value spread is calculated as the ratio between the prices of two shares, measured by their five-day moving average. Even though the two securities in a spread are issued by a single economic enterprise, they can behave differently because of variables such as economic interest, voting and dividend rights, liquidity and currency.

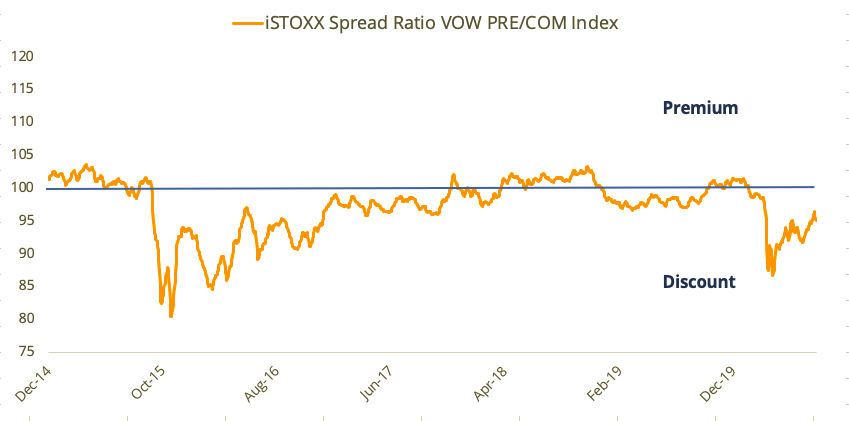

Therefore, some spreads can fluctuate over time. Figure 1 shows the relative spread value of Volkswagen’s preferred shares over the carmaker’s common stock. The blue line at the 100 level represents the level when the two securities trade at parity.

Figure 1 – Spread ratio Volkswagen Preferred/Common

“The iSTOXX Spread Ratio Indices are the latest example from Qontigo of how an index-based solution allows investors and traders to put in place a market strategy with significant advantages in terms of implementation and costs,” said Christoph Gackstatter, Senior Index Product Developer at Qontigo. “We are excited to innovate once again with a new index concept that provides a systematic, rules-based and transparent approach.”

Analysis of pairs

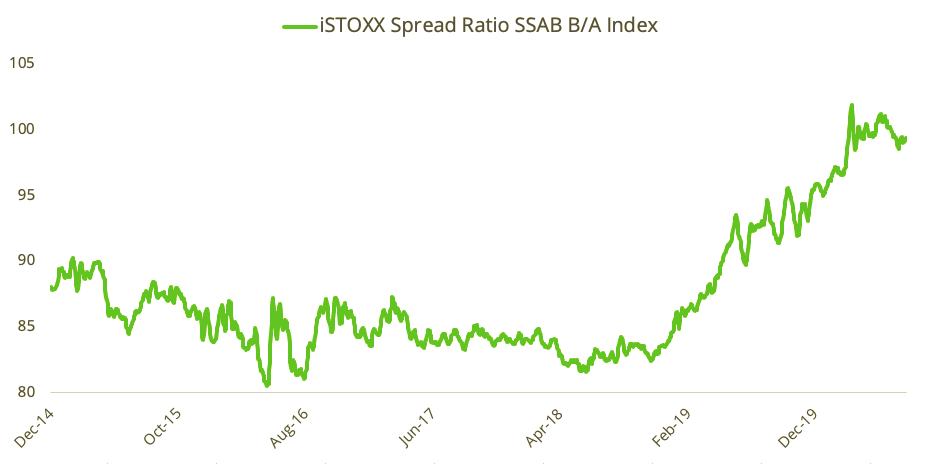

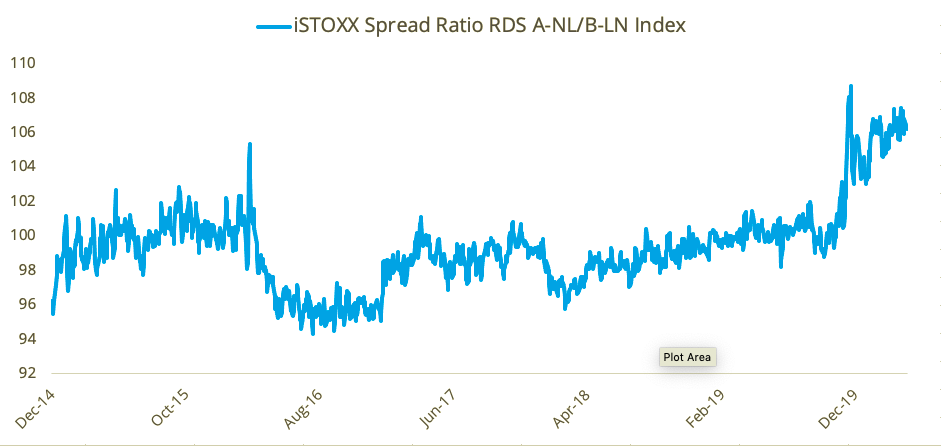

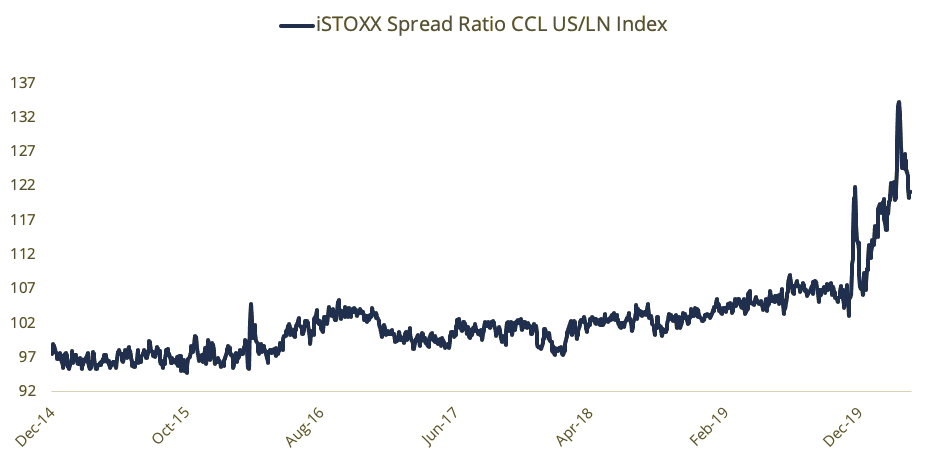

Figures 2 to 4 show iSTOXX indices tracking the spread ratio between securities issued, respectively, by SSAB, Royal Dutch Shell and Carnival. In these cases, the spread has recently moved markedly.

Figure 2 – Spread ratio SSAB B/A

Figure 3 – Spread ratio Royal Dutch Shell A-NL/B-LN

Figure 4 – Spread ratio Carnival US/LN

Other iSTOXX spread ratio indices cover dual listings of Maersk, BMW, Rio Tinto, Liberty Global, Telecom Italia and Volvo.

Advantages of index-based trading

According to Nicolae Raulet, derivatives product developer at Eurex, executing a spread trade with physical shares exposes end users to market moves, requires sophisticated execution systems and has high trading and holding costs. Futures replace the need to transact two stock legs simultaneously, including one that involves borrowing shares to open a ‘short’ position.

Additionally, the physical trade may require a regular currency hedge when the securities are listed in jurisdictions with different currencies. With an index, the spread is automatically adjusted for currency moves during its daily calculation process and these don’t affect the ratio.

Equal notional spread exposure

Another benefit of trading the spread through futures is that the position’s notional value doesn’t change. The holder is only exposed to the profit and loss stemming from variations in the spread, but, unlike the case with cash shares, they are not liable for the increasing or decreasing market value of the position’s constituents.

Finally, Eurex futures have on-screen prices provided by market makers, which allows users to leave limit orders at set spread levels.

“Trading through on-exchange futures eases execution, brings down costs and provides an FX-neutral exposure,” Raulet at Eurex said in an interview. “The futures also bring transparency in terms of an independent mark-to-market valuation, and they substantially reduce counterparty risk.”

“Our key priority is to make end users aware of the added benefits of the new, listed alternative and provide clear, transparent information on key product features,” he added.

1 The family includes 30 unique pair trades, 12 for which there is also an additional index tracking the inverse spread of the same securities.