Stocks posted their first monthly decline since January during September as rising prices from food to energy stoked concerns that central banks may have to raise interest rates just as an economic recovery is losing steam.

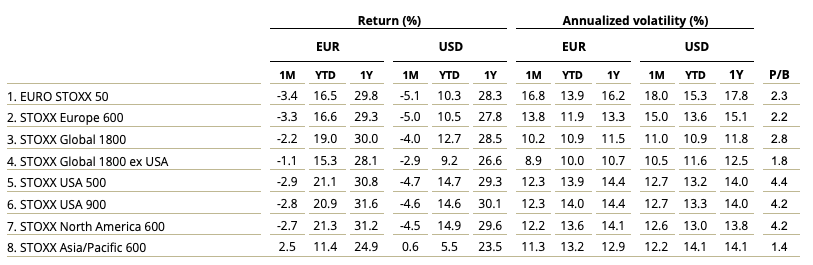

The STOXX® Global 1800 Index fell 4% when measured in dollars and including dividends, its worst monthly showing since the COVID-19 pandemic wreaked havoc in markets in March last year.1 The index dropped 2.2% in euros in the month as the greenback strengthened 1.8% against the euro.

The pan-European STOXX® Europe 600 Index lost 3.3% from a record in euros in the month, while the Eurozone’s EURO STOXX 50® Index decreased 3.4%.2 The STOXX® North America 600 Index slid 4.5% in dollars. The STOXX® Asia/Pacific 600 Index bucked the trend by increasing 0.6%.

Figure 1 – Benchmark indices’ September risk and return characteristics

| For a complete review of all indices’ performance last month, visit our September index newsletter. |

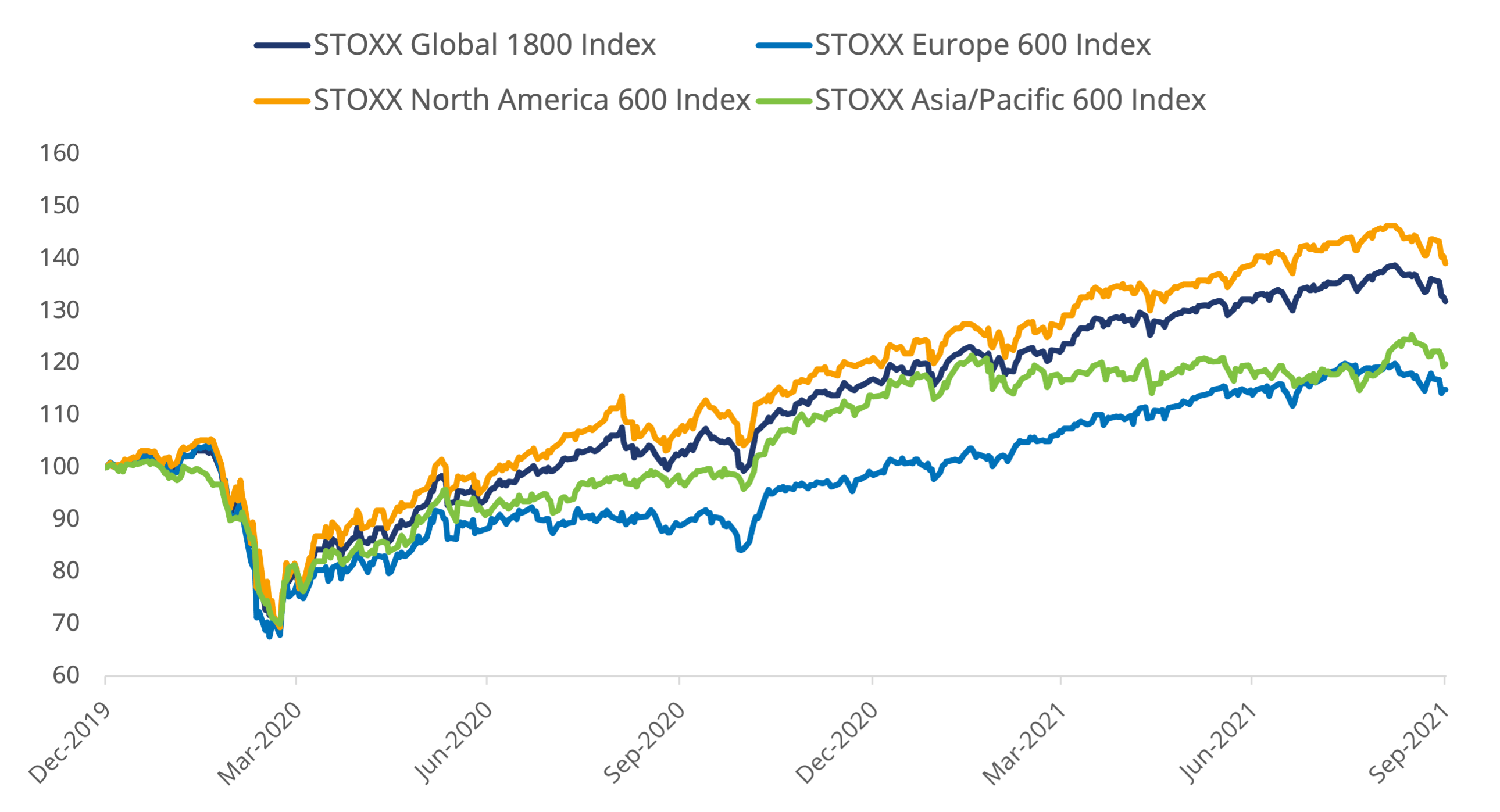

The STOXX Global 1800 has risen 12.7% so far in 2021, headed for its ninth annual advance in the past ten years. The index has posted a yearly average gain of more than 13% over the period.

Figure 2 – Returns since Jan. 1, 2020

Federal Reserve Chair Jay Powell indicated on September 22 that the central bank may start withdrawing monetary stimulus in November and may raise the key interest rate as early as 2022 amid signs that a spike in inflation could last longer than previously anticipated. The yield on ten-year US Treasury notes rose to a three-month high last month. In the Eurozone, a reading of economic activity derived from a poll of purchasing managers fell to a five-month low in September, according to IHS Markit, even if it still signaled expansion.

Volatility rises

The EURO STOXX 50® Volatility (VSTOXX®) Index, which tracks EURO STOXX 50 options prices, rose to 23.2 at the end of last month from 18.8 in August. A higher VSTOXX reading suggests investors are paying up for puts that offer insurance against stock price drops. The index climbed to 86 in March 2020 as countries restricted work and social activities.

Developed and emerging markets

All but three of 25 developed markets tracked by STOXX fell during September when measured in dollars. The STOXX® Developed Markets 2400 Index declined 4% in dollars and 2.2% in euros.

Fifteen of the 21 national developing markets dropped in the month on a dollar basis. The STOXX® Emerging Markets 1500 Index slid 2.8% in the US currency and 1% in euros.

Energy on top

All but three of 20 Supersectors in the STOXX Global 1800 declined in the month. The STOXX® Global 1800 Basic Resources Index (-9.8%)3 occupied the worst rank for a second consecutive month. At the other end, the STOXX® Global 1800 Energy Index (+8.1%) led gains as US oil prices jumped to $75 a barrel during the month from $68.5 in August.

Momentum factor leads losses

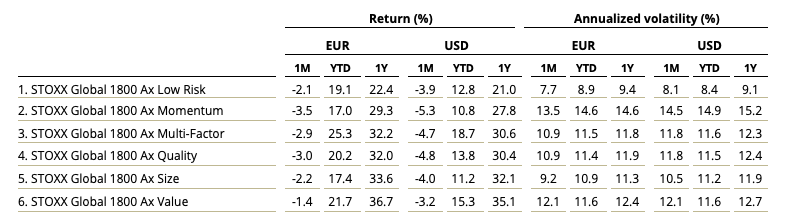

Momentum took a hit during September, according to the STOXX Factor Indices covering global markets. The STOXX® Global 1800 Ax Momentum Index fell 5.3%. The STOXX® Global 1800 Ax Value Index yielded the smallest loss of the group during the month, falling 3.2%.

Figure 3 – STOXX Factor (Global) indices’ September risk and return characteristics

On a regional basis, the steepest losses within factor indices occurred in the STOXX® Europe 600 Ax Momentum Index (-6.8%) and STOXX® USA 900 Ax Quality Index (-6.1%). In Asia/Pacific, all factors logged a positive return except for the STOXX® Asia/Pacific 600 Ax Momentum Index (-1.6%).

The STOXX® Global 1800 ESG-X Ax Momentum Index (-5.5%) led losses among the Global ESG-X Factor Indices. These apply the same factor approach as the Global Factor Indices but additionally exclude companies involved in controversial activities from a sustainability point of view.

ESG-X and ESG integration indices

The STOXX® ESG-X indices, which are versions of traditional, market-capitalization-weighted benchmarks that observe standard responsible exclusions of leading asset owners, had similar performances to benchmarks during the month. The STOXX® Global 1800 ESG-X Index retreated 4%.

Within indices that combine exclusions and ESG integration, the EURO STOXX 50® ESG Index (-2.9%) outperformed its benchmark by 44 basis points. The DAX® 50 ESG Index (-3.5%), which excludes companies involved in controversial activities and integrates ESG scoring into stock selection, performed in line with the benchmark DAX® (-3.6%).

Sustainability indices

Among other families in the STOXX sustainability index framework, the STOXX® Global 1800 ESG Broad Market Index lost 4.1%. The STOXX ESG Broad Market Indices apply a set of compliance, product involvement and ESG performance exclusionary screens on a starting benchmark universe until only the 80% top ESG-rated constituents remain. Companies that are non-compliant based on Sustainalytics’ Global Standards Screening assessment, or are involved in controversial weapons, are not eligible for selection. Additional filters exclude companies involved in tobacco production, thermal coal and military contracting.

Next, the STOXX® Global 1800 ESG Target Index lost 4% in September, the EURO STOXX® ESG Target Index dropped 3.1% and the DAX® ESG Target Index decreased 3.5%. The STOXX and DAX ESG Target Indices seek to significantly improve the benchmark portfolio’s ESG profile while mirroring its returns as closely as possible. The indices follow a similar initial selection methodology as the STOXX ESG Broad Market Indices. From that selection pool they implement, through a series of constraints, an optimization process to maximize the overall ESG score of the portfolio while constraining the tracking error to the benchmark.

The STOXX® Global 1800 ESG Target TE Index, meanwhile, fell 4.1% last month and the EURO STOXX® ESG Target TE Index slid 3%. The STOXX ESG TE Indices follow a similar methodology to the ESG Target Indices, but the optimization imposes a tracking error minimization, subject to a constraint of improving the ESG score of the resulting portfolio.

Finally, the STOXX® Global 1800 SRI Index dropped 4.4%. The STOXX SRI indices apply a rigorous set of carbon emission intensity, compliance and involvement screens, and track the best ESG performers in each industry group within a selection of STOXX benchmarks. In the month that ended, the SRI indices produced returns that topped those of benchmarks.

Climate benchmarks

There were weak performances from the STOXX Paris-Aligned Benchmark Indices (PABs) and the STOXX Climate Transition Benchmark Indices (CTBs). The STOXX® Global 1800 PAB Index and the STOXX® Global 1800 CTB Index both dropped -4.7%. The indices were introduced last year and follow the requirements outlined by the European Commission’s Technical Expert Group (TEG) on climate benchmarks.

Among the STOXX Low Carbon Indices, the EURO STOXX 50® Low Carbon Index (-2.6%) beat the EURO STOXX 50 by 75 basis points last month. Elsewhere, the STOXX® Global Climate Change Leaders Index (-4.6%), which selects corporate leaders that are publicly committed to reducing their carbon footprint, returned 55 basis points less than the STOXX Global 1800 Index.

Housing construction leads losses among thematic indices

The STOXX® Thematic Indices had mixed performances last month. The indices seek exposure to the economic upside of disruptive global megatrends and follow two approaches: revenue-based and artificial-intelligence-driven.

All but three of 22 revenue-based thematic indices trailed the STOXX Global 1800 Index during September. The STOXX® Global Housing Construction Index was the month’s worst performer after shedding 6.8%.

All three STOXX artificial-intelligence-driven thematic indices, on the other hand, beat the benchmark STOXX Global 1800 Index in September. The STOXX® AI Global Artificial Intelligence Index and its ADTV5 version both fell 2.5%, while the iSTOXX® Yewno Developed Markets Blockchain Index dropped 2.7%.

Dividend strategies

Dividend strategies also showed negative returns in the month that ended.

The STOXX® Global Maximum Dividend 40 Index (-5.1%) selects only the highest-dividend-yielding stocks. The STOXX® Global Select Dividend 100 Index (-3.9%), meanwhile, tracks companies with sizeable dividends but also applies a quality filter such as a history of stable payments. The STOXX® Global ESG-X Select Dividend 100 Index (-3.7%) was introduced last February and targets the highest-yielding stocks within universes screened for responsible investment criteria.

The STOXX® Global Select 100 EUR Index, which blends increasing dividend yields with low volatility and is calculated in euros, retreated 1.4%.

Minimum variance

Minimum variance strategies had weak returns in European markets last month, relative to benchmarks. The STOXX® Europe 600 Minimum Variance Index fell 5.4%, while its unconstrained version declined 4.7%.

The STOXX Minimum Variance Indices come in two versions. A constrained version has similar exposure to its market-capitalization-weighted benchmark but with lower risk. The unconstrained version, on the other hand, has more freedom to fulfill its minimum variance mandate within the same universe of stocks.

1 All results are total returns before taxes unless specified.

2 Throughout the article, all European indices are quoted in euros, while global, North America, US, Japan and Asia/Pacific indices are in dollars.

3 Figures in parentheses denote last month’s gross returns.