The recent release of the Axioma Macroeconomic Projection Equity Factor Risk Model (henceforth “macro model”) highlights the risk and return impact of economic variables on equity strategies. Quantitatively driven portfolios are usually constructed (and invested in) without considering the potential impact of big moves in economic variables. We are now experiencing higher term spreads and break-even inflation forecasts, which the Applied Research team has chronicled in several blog posts[1], so the question is quite timely. In fact, as we demonstrate here, the impact of economic variables is relevant more often, and across a broader range of investment strategies, than one might think.

In a recent post focused on equity indices, Inflation. Commodities. Term Spreads: New Macro Model Highlights Their Return Contribution, we used the Macro Model to examine the impact of certain economic and style-factor variables on returns to the STOXX Global 1800 Ax Low Risk index in January and February 2021. In this post we extend the analysis back in time and across three more indices. We revisit the STOXX Global 1800 Ax Low Risk, and add the corresponding Value, Momentum and Quality indices, all compared with the STOXX Global 1800 index. We then analyze the active risk and return contributions starting in 2012.

We show that macroeconomic factors have a far bigger average impact on the risk of the Low Risk and Value indices as compared with Momentum and Quality. The contribution to risk varies over time, and can occasionally be quite high even for the Momentum and Quality indices. And when the economic variables in the model change, as they did in 2020 and again this year, the impact on return can be substantial.

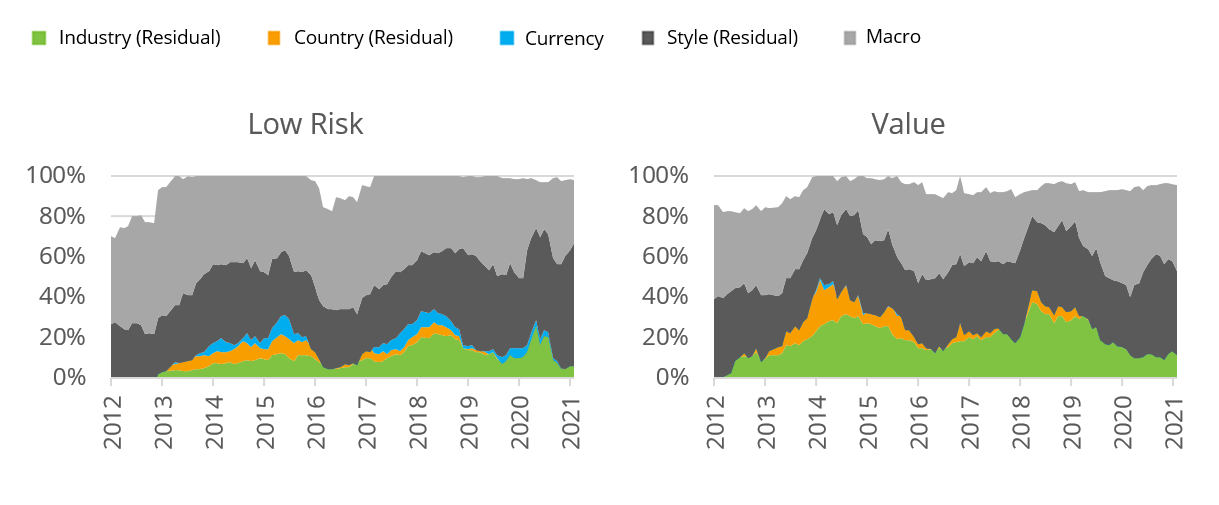

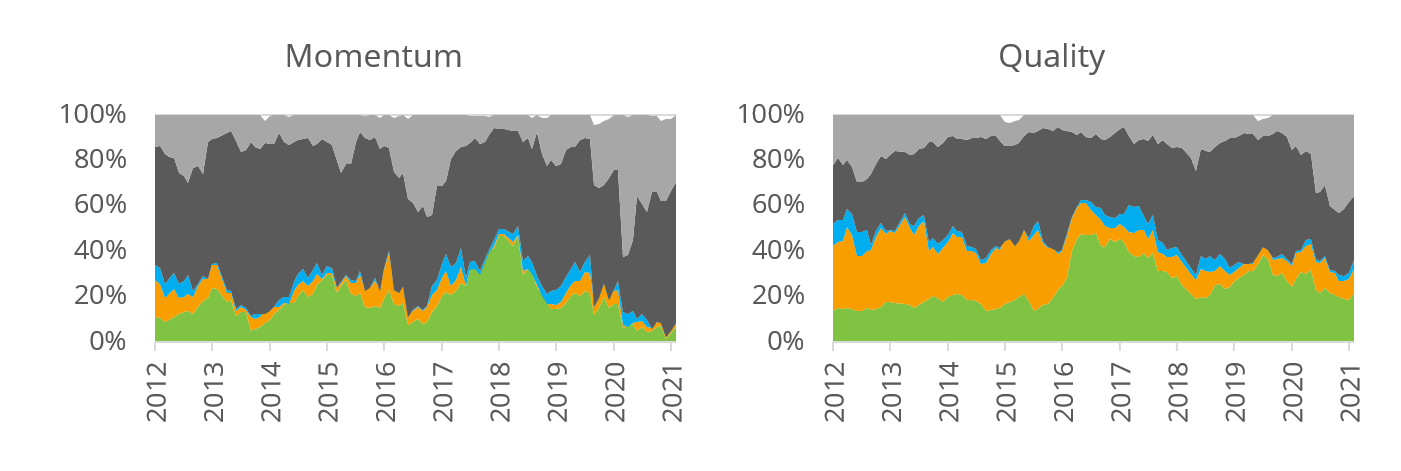

Figure 1 details the aggregate active risk contribution (as a percent of the total active variance) to total factor risk of the macro variables[2], residual contributions of the style, industry and country exposures, and those of currency exposures. Contributions are calculated with the factors’ covariances distributed[3]. Remember that the model starts with the standard fundamental factors (style, industry and country) in our medium-horizon Worldwide model (WW4) and projects them onto the macro factors. The residual returns of the fundamental factors, along with the macro factor returns, are used in the risk calculation.

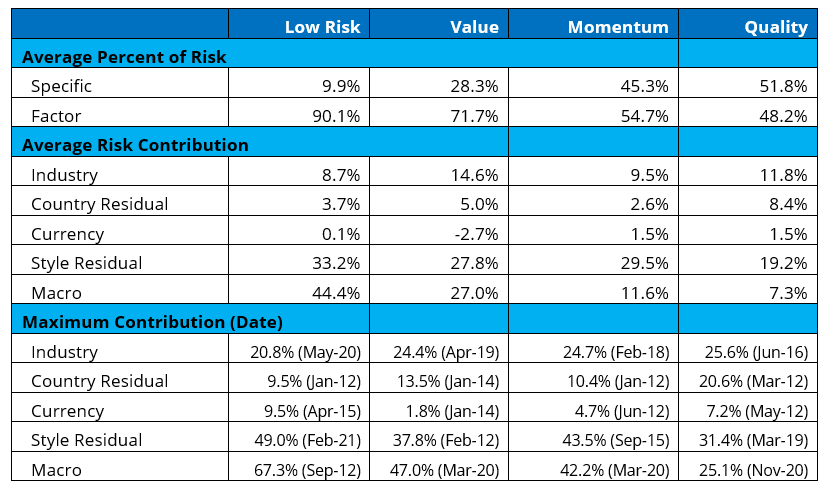

Figure 2 details the average contributions over the period from January 2012 through February 2021, and the month and year when each factor block reached its maximum value.

Is it style or is it the economy?

All the sample indices tilt on one or more style factors, but the factors can be correlated with those coming from the macro model—hence what is classified as style risk using a standard model may actually fall into the macro-risk category[4].

Eyeballing the sand charts, and confirming with the data in the table, we see that over time, macro factors accounted for much more of the risk of the Low Risk and Value indices than they did for Momentum and Quality. In turn, factor risk in aggregate was much higher for Low Risk and Value than it was for Momentum and Quality. But it is also clear that macro risk periodically plays an important role. In the Quality index, macro risk accounted for 25% of the total active risk in November 2020, and it contributed 47% and 42%, respectively, for Value and Momentum as the market tanked in March 2020. Macro risk is clearly an important data point for all types of portfolios.

Figure 1. Contribution to Factor Risk

Figure 2. Risk Statistics, 2012 – February 2021

If it contributes to risk, it will contribute to return…

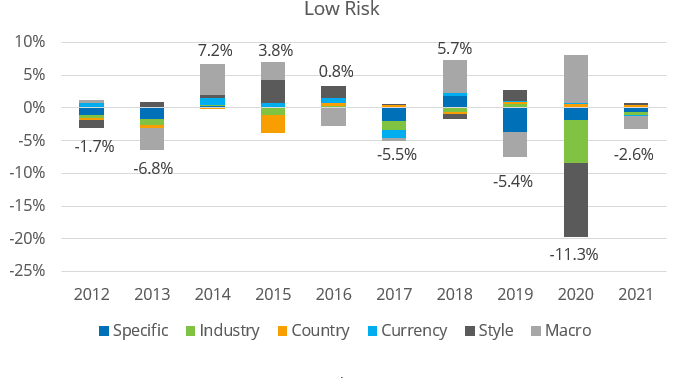

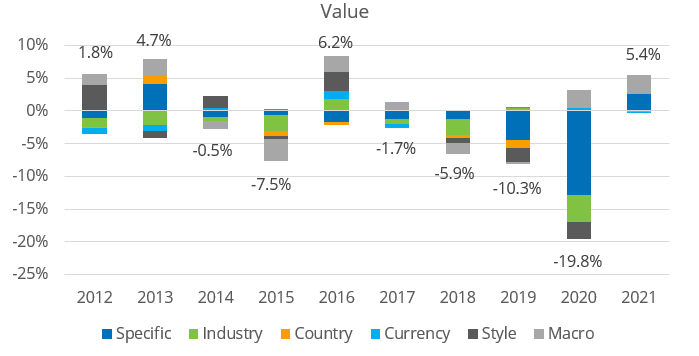

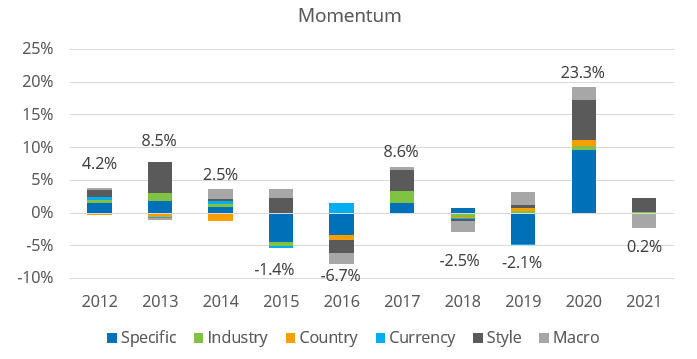

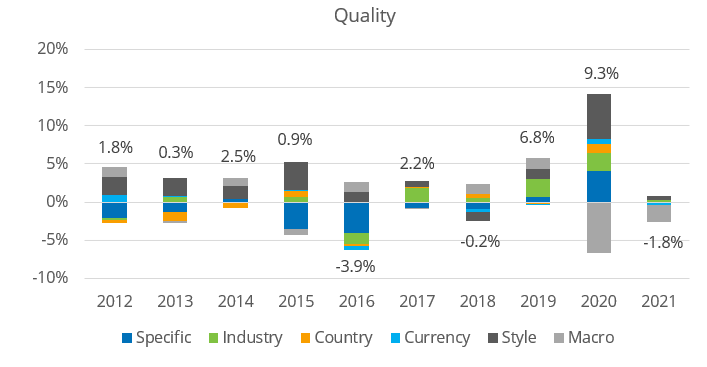

Now we turn to the impact of macro and other factor blocks on return. Figure 3 shows the year-by-year breakdown of factor block contribution to active return, with the actual active return above (for positive) or below (for negative) the bar for that year5.

Of course, we would expect to see factors with a bigger contribution to risk account for a higher proportion of return. To be sure, that is the case for the Low Risk index. For most years, macro and style factors were the biggest contributors to the overall active return, often with one the highest and the other the lowest. Using a standard risk model may ignore this macro impact, as the returns might be put in the industry, country or (most likely) style bucket, and the relationship between the portfolio’s holdings and the macro economy may be lost. Macro factors also contributed significantly to Value’s active returns; in most years, the magnitude of macro contributions was higher than that of most other factors. As for the Low Risk index, this is to be expected, as (along with style factors) they accounted for a high proportion of the risk.

The impact of the macro factor exposures on Momentum was smaller than it was for Low Risk and Value. Still, it was often significant, with a contribution more than 1% or less than -1% in six of the nine full years of the study. With the macro upheaval in the first two months of this year, macro factors led to a 2% drag, almost completely offsetting the positive impact of the index’s Value exposure.

Finally, Quality, for which macro exposure increased substantially starting in 2020, saw an extremely large negative impact (-6.7% contribution) from those exposures in 2020, and another -2.2% impact so far in 2021. Macro factors were the major source of the index’s underperformance this year.

Figure 3. Annual Active Return Contribution by Factor Block

Source: Qontigo

Conclusion

Many portfolios, especially those that are quantitatively driven, do not take the macroeconomy into account when constructed. While the standard model and the macro model will produce the same portfolio (remember, the risk is the same, it is just its breakdown that differs), the manager or asset owner may want more insight into the sources of those returns. Even when the average macro exposure is small, there are periods when those exposures can have a large impact on risk and performance. Often what we think of as factor contribution—for example, from the Leverage style factor, which has a negative exposure in the Quality portfolio—is actually tied to what is happening in the economy, such as the impact of falling rates in early 2020, which likely helped the return of Leverage and therefore hurt Quality owing to the negative bet.

The macro model could be used in portfolio construction (say, to minimize exposure to certain economic variables, such as falling rates). But even absent that, use of it can be critical in determining why a portfolio fared the way it did—and, in the process, shed light on the previously unconsidered economic impact, especially to the style factors on which the portfolio tilts.

For more insights and research from the Applied Research team, please click here.

[1] See, for example, “When ‘good’ inflation becomes ‘bad’ inflation – 2018 reloaded”, “Anxious about rising yields and inflation? Here’s why (perhaps) you should be…” and “Inflation. Commodities. Term Spreads: New Macro Model Highlights Their Return Contribution” among others.

[2] We do not break out the individual variables in this short post, but please contact your Qontigo representative for more detail.

[3] Where they do not add to 100 it is because one or more factor blocks, usually Currency, is negatively correlated with the others and therefore provides a diversification benefit.

[4] The same may be true for industries and countries, but they tend to account for a much smaller portion of the risk for these indices.

[5] We show the year-by-year data because summary data for the full period obscures the occasional large contribution in a single period that might be offset by a contribution in the opposite direction in the next.